Rob McDonough and I coauthored an article in April of 2023 concerning Silicon Valley Bank (https://www.gfmi.com/articles/silicon-valley-bank-interest-rate-and-liquidity-risk-within-asset-liability-management/), their interest rate and liquidity policies, and the reasons for their demise. What has changed since the March banking crisis? Let’s take a look at the current interest rate environment, what challenges may be looming during this scariest of scary months, and what were some of the conclusions of the regulators reports on the banking crisis of 2023.

Today’s Environment

The main reasons attributed to the 2023 banking crisis are the losses on the investment portfolio and the almost instantaneous (a.k.a. social media) withdrawal of uninsured deposits (clearly this “run on the bank” was a major cause for the crisis; however, this article focuses more on the investment portfolio). The losses on the investment portfolio were caused by the significant increases in interest rates. Let’s take a look at the current economic environment including GDP, Fed Funds, the 10-year U.S. Treasury, inflation, and the U.S. Dollar. Once this brief analysis is complete, we can come to a conclusion on the current state of the investment portfolios.

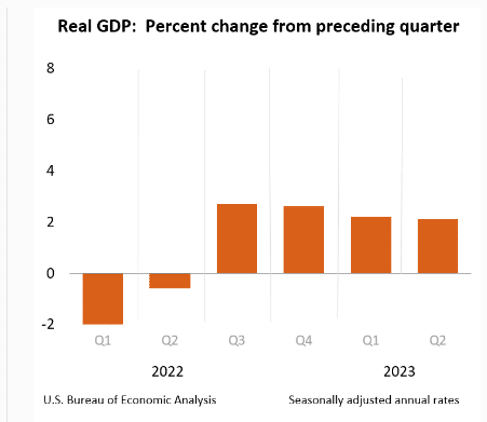

GDP

Despite the inverted yield curve, which is a good predictor of a recession, along with market participants’ perceptions of heading into a recession, the U.S. economy has been resilient. Chart 1 shows GDP hovering above 2% over the last couple of quarters. Clearly the economy is not in a recession.

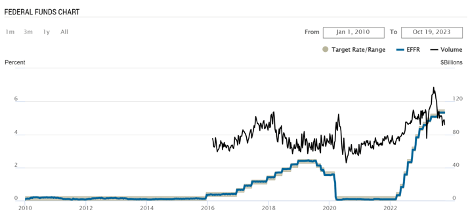

In Chart 2, we can see the Fed Funds target was 0.00 – 0.25% from 2010 to 2016. The Fed then clearly raised the target, started lowering it in mid-2019 and then of course the pandemic hit. The target range was back to 0.00 – 0.25% and then as we all know inflation started ratcheting up. From the end of the first quarter 2022, the Federal Reserve became very aggressive raising rates. As of this writing, the Fed’s target range is 5.25 – 5.50%. Most pundits predict one more 25 basis point increase before the end of the year.

The USD was making multi week highs (see Chart 3) and has now taken a breather. This is an indication the FX markets believe the spread between short-term U.S. interest rates and other countries’ short-term rates is increasing, thereby attracting capital flows into the U.S. This potentially implies market participants believe the Fed will continue to raise short-term rates.

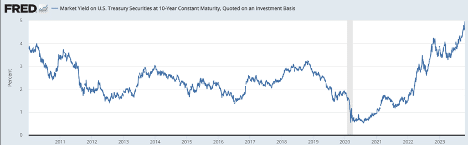

Analyzing Chart 4, the 10-year U.S. Treasury hit a low of 0.57% in August of 2020. On March 3, 2022, the rate was 1.86%. As of this writing it is about to breach 5%! (In my opinion the next stop is 5.15 – 5.25%). That is over 300-basis point move from the banking crisis earlier this year! Investment portfolios, assuming there was no hedging, could not have performed very well.

Chart 4

Source: Board of Governors of the Federal Reserve System (US), Market Yield on U.S. Treasury Securities at 10-Year Constant Maturity, Quoted on an Investment Basis [DGS10], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/DGS10, October 21, 2023.

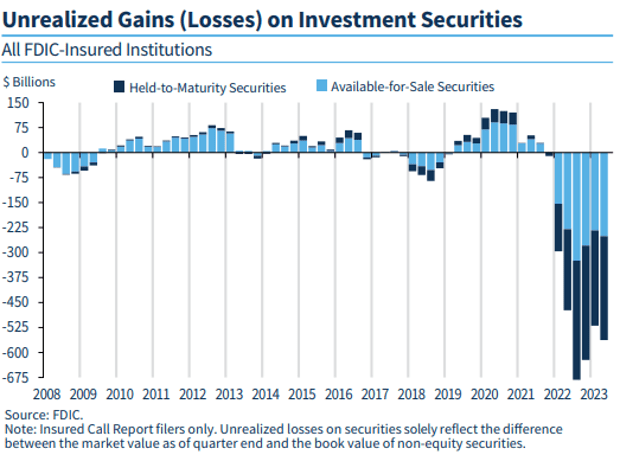

FDIC Estimates of Investment Portfolio Losses

Following in Chart 5 the FDIC is illustrating banks’ investment portfolio losses at the end of Q2 2023.

Losses on securities were up by $42.9 billion or 8.3% from the first to second quarter in 2023 as the chart indicates.1

Challenges in Today’s Landscape

U.S. Government, U.S. Government Debt and FX Markets

The current situation in the U.S. House of Representatives remains an unknown. Markets do not like uncertainty. On top of that, the budget will have to be passed, AGAIN, in less than 30 days. S&P and FitchRatings have already lowered the credit rating on the U.S. and Moody’s has talked about following suit.

According to the WSJ2 more than half the government debt will roll over within three years. Further, the article goes on to state, “The largest spending increase this year was the cost of the government paying for its debt. The Treasury spent $711 billion on net interest payments last fiscal year, an increase of $177 billion, or 33%, from fiscal year 2022, according to CBO.”

The FX markets seem to have brushed this off as the USD continues to get stronger indicating market participants have full confidence in the US Dollar.

Banks Cost of Funds

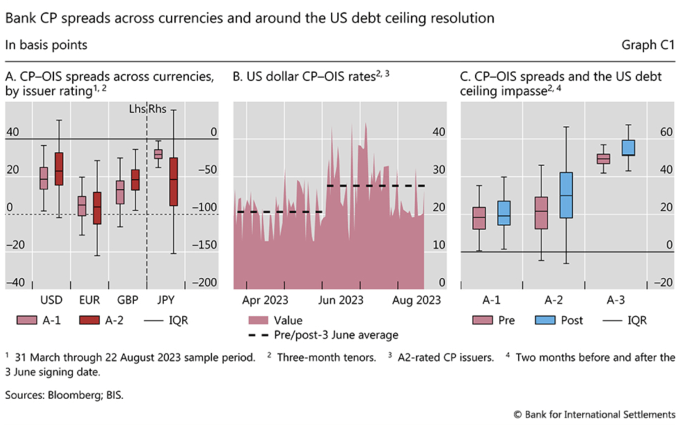

Although there is no more TED Spread (Treasury-EuroDollar spread historically was a good indication of stress in the funding markets), the BIS had an interesting piece on the bank Commercial Paper rate vs OIS (Overnight Index Swap). The following graph shows the spread widening, i.e., higher cost of funds for banks during the June 2023 budget agreement/debt ceiling. To clearly see this, focus on panels B and C in Chart 6.

The Fed has already raised rates and is looking to potentially raise rates again. If banks’ cost of funds increase further as the BIS analysis might indicate, the cost of carry of the investment portfolios will increase which will further negatively impact banks’ earnings. This scenario would not be good for the perceived liquidity picture of the banking system, i.e., lower earnings accompanied by further losses in the investment portfolio.

Soft Landing

The big question is the economy and inflation. Will the U.S. continue at a growth rate of 2%. Will inflation come down enough for the Fed not to raise rates again. Have we seen a top in the 10-year? At this point in time, it doesn’t look pretty and is actually quite scary.

Summary of Actions by the Government

Here is a good summary by the GAO of the crisis in its immediate aftermath:

“On March 12, 2023, the Secretary of the Treasury approved the systemic risk exception, which authorized FDIC to guarantee insured and uninsured deposits of the two banks. FDIC and the Federal Reserve Board assessed that not guaranteeing the uninsured deposits likely would have resulted in more bank runs and negatively affected the broader economy. The Secretary of the Treasury concurred with this assessment and made the determinations.

After determining that additional banks might need support and to minimize financial contagion, the Federal Reserve created the Bank Term Funding Program on March 12, 2023. The program provides eligible banks with additional liquidity by allowing the 12 Reserve Banks to provide loans of up to 1 year. Federal Reserve staff documented how the program met the requirements for an emergency lending facility under section 13(3) of the Federal Reserve Act, and Treasury approved the program.”3

The BTFP is still available today with approximately $121 billion outstanding as of August 31, 2023.4

The Fed produced a report on Silicon Valley Bank5. Here are the “Issues for Consideration” found in the report:

“This report identified a number of issues relevant for how the Federal Reserve designs and implements its supervisory and regulatory program. As discussed throughout the report, the failure of SVBFG reflects a complex interaction of many factors, some of which were idiosyncratic to the management and business model of SVBFG and how oversight was executed, while others were broader, with the potential to impact the effectiveness of the oversight program.

The observations are organized around four broad themes: (1) enhance risk identification, (2) promote resilience, (3) change supervisor behavior, and (4) strengthen processes. The ideas are meant to be feasible in that they fall within the Federal Reserve’s existing authorities and support the Federal Reserve’s existing mandates. These are not full-fledged proposals and are not intended as a checklist of specific actions. Rather, they represent ideas that may warrant further consideration by policymakers based on observations related to the failure of SVBFG and broader environmental changes, such as technological innovations that impact the pace of financial flows. Many options involve difficult trade-offs that must be considered carefully by policymakers; e.g., a more forceful oversight program may increase resilience but may also add burden or hinder financial intermediation.”

Conclusion

This article has reviewed the current market environment, the impact on investment portfolios, and some actions and insights from the government and regulators since the crisis. Clearly there are more losses in the investment portfolios as interest rates have risen since March of this year. Hopefully, asset liability committees (ALCO) have discussed and taken action on one of the oldest challenges in banking: profitability versus liquidity and have hedged some of their investment portfolio positions. From a liquidity risk perspective, there are many considerations other than the investment portfolio, some of which include ratio analysis, identifying stickiness of deposits, understanding the relationship between liquidity, credit and interest rate risk, liquidity stress testing, and contingency funding plans. The liquidity supervisory and regulatory landscape is sure to change in the future. Hopefully between now and then we do not experience an October scary or indeed, in any month to come!

Ken Kapner, CEO and President, started Global Financial Markets Institute, Inc. (GFMI) a NASBA certified financial learning and consulting boutique, in 1998. For over three decades, Ken has designed, developed and delivered custom instructor led training courses for a variety of clients including most Federal Government Regulators, Asset Managers, Banks, and Insurance Companies as well as a variety of support functions for these clients. Ken is well-versed in most aspects of the Capital Markets. His specific areas of expertise include derivative products, risk management, foreign exchange, fixed income, structured finance, and portfolio management. He has been a Risk Management Advisor to a Mutual Fund’s Board of Trustees and has served as an Expert Witness using knowledge of derivatives, trading and risk management.

Prior to starting GFMI in 1998, Ken spent 14 years with the HSBC (Hong Kong and Shanghai Banking Corporation) Group in their Treasury and Capital markets area where he traded a variety of instruments including interest rate derivatives, spot and forward foreign exchange, money markets; managed the balance sheet; sat on the Asset Liability Committee; and was responsible for the overall Treasury activities of the bank. He later headed up HSBC’s Global Treasury and Capital Markets Product training for two years in Hong Kong. Specifically, his responsibilities included developing new courses and delivering courses to traders, support staff and relationship managers. In New York, he established a training department for the firms’ Securities Division where he was in charge of the MBA Associates Program, continuing education and Section 20 license.

He has co-authored/co-edited seven books on derivatives including The Swaps Handbook and Understanding Swaps.