In March of 2020, an anomaly in a relatively obscure part of the U.S. Treasury bond futures market caused a major disruption in that market, which in turn prompted the U.S. Federal Reserve to put forth $5 trillion of liquidity to calm the markets. Yep, that was “trillion”, with a “t”! At the root of this market disruption was a common trade known as the “cash-futures basis.” By definition, the Treasury Futures basis or “basis” is the price difference between the cash security and the futures contract, also referred to as the spread. The price difference exists because, by design, futures contracts are priced today but delivered at some specified date in the future. To price the futures contract:

- The Treasury note/bond is purchased today.

- The purchase is assumed to be financed with borrowed money.

- The Treasury is then held or “Carried” to the maturity date of the futures contract.

- The owner of the bond during this “carry” period earns the coupon from the Treasury.

- The difference between the cost of financing and the return earned on owning the note/bond is called the “cost of carry”. This cost of carry is added/subtracted to the cash price of the Treasury security to obtain the price of the futures contract.

Now that the fundamentals of the basis have been explained, let’s examine the forces driving that anomaly, and discuss some of the implications for the capital markets. We begin with a brief description of the settlement process of Treasury futures trades.

When Treasury futures are fulfilled by physical delivery, they need to meet the contract specifications which define the deliverable grade Treasury securities. In addition, they are delivered at the contract delivery invoice price. There are multiple categories of Treasury Note and Bond futures, with each category corresponding to a defined maturity range of outstanding Treasury securities eligible for good delivery. For instance, the 10-Year Note (ZN) futures contract has a size of $100,000, and Deliverable Grade of Treasury Notes with maturities ranging between 6½ to 10 years. 1

A list of Deliverable Grades, labeled Deliverable Maturities in the table, for Treasury Note and Bond Futures is outlined in the following table:1

As you can see, each futures contract has a defined range of maturities for different outstanding Treasury securities which can serve as deliverable for satisfaction of that futures contract. A unique feature for U.S. Treasury futures is that the short seller of the futures contract may choose any day in the month that the futures contract matures to deliver the security versus a single date in which the security must be contractually delivered. The actual delivery process consists of actions on three distinct dates for each contract:

- Intention Day, the day on which the short futures position holder (the “short”) notifies the Exchange of their intention to deliver;

- Notice Day, the day (one day following Intention Day) that an invoice is prepared by the short futures position holder specifying the exact securities to be delivered by the long futures position holder (the “long”) in exchange for the sale price; and

- Delivery Day, on which the short’s clearing firm must deliver the securities, and the long’s clearing firm must deliver payment.2

As the long contract holder’s clearing firm is contractually obligated to accept the seller’s decisions during the contract month, the seller of the futures contract in effect holds an American style option during the delivery month that includes two benefits: timing of delivery and choice among different Treasury securities qualifying for good delivery under that contract. Prior to futures expiration, all parties in the transaction will monitor all issues eligible for delivery under the contract in order to identify which security is “cheapest to deliver” or CTD. CTD is the security “for which the corresponding futures delivery invoice amount is largest relative to the issue’s all-in-price for spot settlement in the cash market” (page 5).2

In mid-March of this year, with the dramatic rise in coronavirus cases around the world, investors rushed into Treasuries as the safest available investment and did so through the futures market rather than purchasing Treasuries outright. The futures market offered greater liquidity as well as the use of leverage. However, the rush into the more liquid futures market caused the spread between futures and Treasuries to grow much wider. Furthermore, the spread widened “between 2-year bonds linked to futures and those that aren’t.” 3 The following description of the trade appeared in Bloomberg on March 17:

“… when futures diverge from the notes underlying them, investors can buy the ‘cheap’ bonds and sell the futures to pocket the difference. The spreads between the two are usually tiny so funds use cash borrowed from the repurchase market to leverage up positions and boost returns.” 3,4

The article went on to indicate that exposure to this strategy could have been as high as $650 million according to a note from JPMorgan Chase strategists.

Source: Bloomberg 3

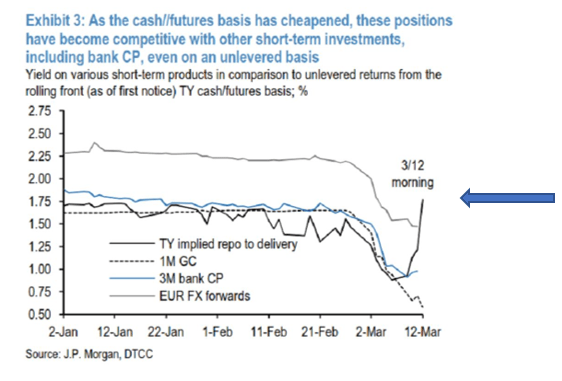

Larger, unleveraged investment funds were also attracted to this trade and began diverting investments from commercial paper into the Treasury futures trade, which by comparison is nearly risk-free. Specifically, short term investors will sell the Treasury futures contract short and buy the underlying Treasury. Upon maturity of the futures contract, the investor delivers the security. The difference between the cash outflows from purchasing the security and cash inflows from delivering the security into futures contract will result, in this case, in a short-term rate of return. This can be compared to other money market instruments. When the return through this strategy is high enough, short term investors will execute this strategy. The rate of return in this market is commonly referred to as the implied repo rate. (A rather unfortunate term as it often gets confused with traditional repos).

Source: Bloomberg 3

This diversion brought substantially more funds into the trade at the expense of liquidity for corporate borrowers who heavily use instruments such as commercial paper. JPMorgan summed it up as follows: “The incentives are quite strong for real money to reallocate away from these markets and into nearly risk-free basis positions at a higher yield…In that sense there is a rather direct channel between stress in the futures basis market and a wide range of other asset classes, including but not limited to unsecured bank funding.” 3 The subsequent massive intervention by the Federal Reserve certainly underscored how the knock-on effects of stress in the futures market can negatively impact real economic activity.

In some respects, this is reminiscent of another well-documented risk management case study in the derivatives markets for Metallgesellschaft AG (“MG”). As many may recall, in 1993, MG sold long term forward contracts and hedged the position by combining a long position in short dated energy futures, specifically following a strategy known as stacking, along with swaps. On the face of it, it looked like the market risks were hedged. But as the market moved from backwardation to contango, the hedge did not perform as advertised. MG ended up losing $1.5 billion dollars! Not exactly the same set of events, but certainly a reminder of how dramatically even seemingly calm and consistent futures markets can suddenly have outsized impacts.

If you want to learn more about the futures, bond and repo markets, as well as many other aspects of the worldwide capital markets, check out our course offerings on https://www.gfmi.com/training-courses/ .

1 https://www.cmegroup.com/trading/interest-rates/basics-of-us-treasury-futures.html

2 Treasury Futures Delivery Options, Basis Spreads, and Delivery Tails, CME Group, September 2016

https://www.cmegroup.com/education/files/treasury-futures-basis-spreads.pdf

3 How a Little-Known Trade Upended the U.S. Treasury Market, Bloomberg, March 17, 2020, Stephen Spratt

https://www.bloomberg.com/news/articles/2020-03-17/treasury-futures-domino-that-helped-drive-fed-s-5-trillion-repo

4 For an explanation of repurchase agreements or repos please go to GFMI’s article:

https://www.gfmi.com/articles/libor-schmibor-whats-next-sofr-part/