The Multiplier Effect and GDP Growth

I came across this table (see below) in a recent Wall Street Journal Blog (WSJ’s Daily Shot: America: Too Many Retirees, Not Enough Workers). Although the article isn’t about fiscal policy per se, I thought the reference to the multiplier effect—or, more specifically, the depiction of the impact of the multiplier over a range of potential fiscal actions—was interesting given potential changes in federal government spending and tax structure with the new administration.

What is a Multiplier?

What is a multiplier or, more specifically, a fiscal multiplier? Let me give you a simple example in layman’s terms: If the government spends a dollar on infrastructure and then subsequently hires new workers, these new workers will have more money to spend. As these new workers in turn spend money, the effect of the original dollar is multiplied. Here’s another example: Let’s say that lots of consumers purchase new appliances. These new appliance purchases would benefit the store where the purchases were made. The appliance store may even need to hire more people if the stimulation from the spending is large enough!

The new president wants to cut taxes across the board and increase spending for infrastructure. Presumably, these tax cuts and increased spending would result in a multiplier effect. However, the precise effect is not yet known. To my knowledge, economists have never agreed upon an exact multiplier, hence the range in the chart above.

Affecting Multiplier Effects

There are so many factors that may impact the multiplier effect, that I have summarized a few of them below:

- By any standard, monetary policy is quite loose. However, if the economy picks up steam, the Fed would potentially begin accelerating their pace of tightening, thereby dampening economic growth and negatively impacting the multiplier effect.

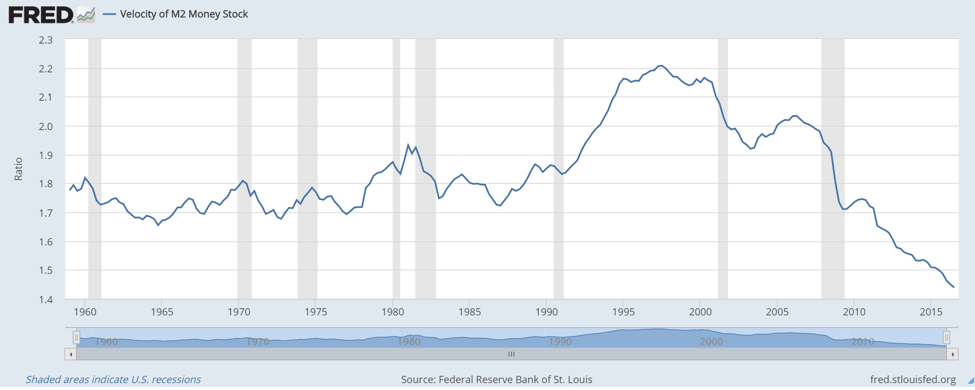

- From a monetary theory viewpoint, velocity is extremely low. How will an increase in government spending impact velocity? If government spending increases GDP and velocity increases, will this result in an increase in the rate of inflation? The chart below from the St. Louis Fed shows how velocity has fallen since the great recession.

- The unemployment number is currently below 5%. Logically, one would think there wouldn’t be much impact here other than driving wages and inflation higher. However, the participation rate has been hovering at historically low levels of approximately 62%. Will government spending bring the participation rate higher without a corresponding increase in inflation? Or will it alternatively drive up inflation?

- It is no secret that the Obama administration tried to increase spending but Congress wanted other cuts in the budget to offset the increase in spending. If the same thought process is brought forward, what specific areas of the budget will be cut? Looking at the multiplier chart, one can see that there will potentially be quite a different, negative impact, on the multiplier depending on what gets cut.

These are just some thoughts to ponder, as we will have to wait to see what impact the new administration’s fiscal policies will actually have.

More Information about the Multiplier Effect

If you are interested in learning more about the multiplier effect and economic policy, GFMI’s own Macroeconomics, Central Banks, and Their Impact on Asset Values course may be right for you. Feel free to contact me to explore training options. As always, thank you for reading!