“When financial markets come under pressure, vital functions such as the efficient allocation of

capital and price formation become impaired.” BIS Quarterly Review, September 2022

Recently, there have been various signs of stress in the U.S. Treasury market. Coincidentally, there were two recent reports released by regulators discussing the Treasury market. The first is the Financial Stability Report by the Board of Governors of the Federal Reserve System1 and the second was released by the Inter-Agency Working Group (IAWG) for Treasury Market Surveillance titled “Enhancing the Resilience of the U.S. Treasury Market: 2022 Staff Progress Report.”2 Both reports were released in November 2022. This blog discusses the stresses in the market and some of the suggestions found in the IAWG report.

Signs of stress in the U.S. Treasury market include:

- Wider spreads between the on-the-run Treasury and off-the-run Treasury. Traditionally this spread is approximately 2 basis points and currently, it is around 8 basis points

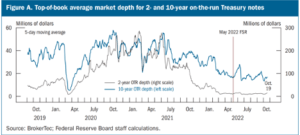

- Reduced amount of average trade size. The following graph indicates the average market depth based on the average trade size based on a 5-day moving average. It clearly indicates a lower trade size. Today’s environment is comparable to the stress the market experienced in March 2020.1

Interestingly, the same report points to the bid-offer spread between the 5- and 10-year on-the-run Treasurys and not necessarily pointing to stress in the market. Generally, the bid-offer spread will widen in times of crisis making trading far more expensive.

To further support the concept of stress in the markets here are a few comments from various sources:

Prudential Global Investment Management (PGIM) Q4 22 Quarterly Outlook

“Liquidity in the bond market continues to worsen and the cost of trading has become surprisingly high, even though market functioning has been gradually deteriorating in the recent past. A liquidity gauge that measures deviations of the U.S. Treasury yield curve from model fair value has deteriorated to a level last seen in March 2020, when the market breakdown was so acute that the Fed had to step in to buy Treasuries. It’s likely that liquidity will continue to deteriorate as quantitative tightening continues to exert pressure on the private sector to absorb Treasuries.”3

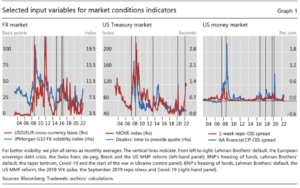

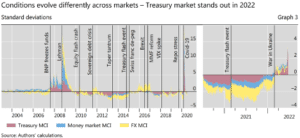

The Bank for International Settlements (BIS) has introduced what they call market conditions indicators: “We introduce market conditions indicators (MCIs) for each of three key market segments: the US Treasury and US money markets, and the foreign exchange market centered around the US dollar. Our daily MCIs reflect market volatility, illiquidity, and deviations from standard no-arbitrage conditions. They capture well-known episodes of market turmoil.”

“The specific variables we consider are well known (online annex Table A). …Measures of market liquidity, in turn, aim to capture the ease with which market participants can trade without significantly affecting prices. Examples include quoted bid-ask spreads for spot FX or the premium between on- and off-the-run Treasury securities. Finally, we incorporate measures of market uncertainty, such as the JPMorgan FX volatility indices and the MOVE index for the FX and Treasury markets, respectively.”4

Following are some selected graphs from the BIS article indicating potential stress in the markets.

The MOVE index in the above graph is defined as U.S. Treasury yield volatility implied by 1-month options on 2-, 5-, 10- and 30-year Treasuries. It is similar in nature to the VIX, which is sometimes called the fear gauge. The VIX measures volatility based on the S&P 500 and the MOVE index measures volatility in the Treasury market.

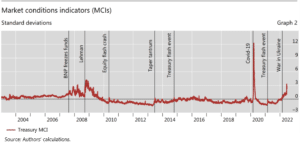

In graph 2, “Positive values reflect tighter than average market conditions.” Note the upward swing in 2022 for the Treasury MCI.

“Comparing the three indicators can shed light on how conditions differed across markets at any given point in time…More recently, tight market conditions were most visible in the Treasury market, with values approaching the levels seen during the GFC (though still well below the Covid-19 turmoil).”

Finally, the repo market is also seeing signs of stress. Some of the on-the-run Treasuries have gone special or commanding a lower interest rate than what would be expected in normal conditions. Here is a quote from PGIM Fixed Income Q4 22 Quarterly Outlook Published in October 2022.3

“Meanwhile, dynamics in the Treasury repo market are also out of the ordinary. Investors who short Treasuries are turning to the repo market to borrow specific securities, causing repos for some on-the-run issues to trade special or even negative. The Fed’s balance sheet runoff will likely exacerbate the specialness of some securities as the supply of on-the-runs at the Fed’s securities lending operations dries up.”

Reasons given for the stress

Here are the reasons often cited for the stress in the U.S. Treasury markets:

- The Federal Reserve’s increase in interest rates, as well as the pace of the increase, to tackle inflation.5

- The Federal Reserve reducing their balance sheet commonly referred to as quantitative tightening or QT5

- Central banks are either not buying U.S. Treasuries or selling them

It is a natural reaction for fixed-income asset managers to either pull back on purchasing fixed-income securities as yields are going higher/prices going lower or simply wait to invest at higher coupons and stash the cash in T-Bills. One-month and 3-month T-Bills are yielding approximately 3.86% and 4.25% respectively. This is not even taking into account the expectation the Fed will increase rates again the next time they meet in mid-December.

Regulator actions to smooth things over

In July 2021 the Fed took two steps to help mitigate potential future stress events in the market. First, they established a Standing Repurchase Agreement (repo) Facility. According to the Fed, the facility serves as a backstop in money markets to support the effective implementation of monetary policy and smooth market functioning.6

Second, they established the Foreign and International Monetary Authorities (FIMA) Repo Facility. According to the Fed, the facility can help address pressures in global dollar funding markets that could otherwise affect financial market conditions in the United States. Its role as a liquidity backstop also helps to support the smooth functioning of financial markets more generally.7

There also have been mentions of the U.S. Treasury, not the Fed, buying back securities.

Recommended reforms to further improve the U.S. Treasury market

The IAWG2 report also has the following recommendations:

- Improving the resilience of market intermediation

- SEC dealer registration proposal

- Market structure – Specifically the recommendation is for All-to-All (A2A) trading to become more widespread in the U.S. Treasury market. In the A2A concept, any market participant can deal with one another and not go through an intermediary. A2A is already a main fixture in the corporate bond market.

- Congruent margin regulation

- Improving data quality and availability

- Evaluating expanded central clearing

- Enhancing trading venue transparency and oversight

- Examining effects of leverage and fund liquidity risk management practices – “…the growing size and influence of certain investor positions and associated trading flows, such as from open-end funds and hedge funds, may amplify stresses in the Treasury market.”

Conclusion

A lot of indicators have pointed to stresses in the U.S. Treasury market. To date, the market seems to be functioning properly. The Fed’s march to higher interest rates and the downsizing of its balance sheet will continue to impact the U.S. Treasury market as well as other major asset classes. One of the lynchpins here may be the U.S. dollar and how global investors react to the weakening/strengthening of the reserve currency. Only time will tell.

References

1 https://www.federalreserve.gov/publications/files/financial-stability-report-20221104.pdf

2 https://home.treasury.gov/system/files/136/2022-IAWG-Treasury-Report.pdf

4 https://www.bis.org/publ/qtrpdf/r_qt2209c.pdf

6 https://www.federalreserve.gov/monetarypolicy/standing-overnight-repurchase-agreement-facility.htm

7 https://www.federalreserve.gov/monetarypolicy/fima-repo-facility.htm