Introduction

Economic fundamentals, supply chain issues, and energy prices have all contributed to interest rates moving higher. The Fed started raising rates in March of this year to combat the rise in inflation. The 10-year US. Treasury started the year around 1.53%, and at this writing is at 3.35%. (Note the TNX is a CBOE index where 33.50 = 3.35%)

However, hedging a portfolio sensitive to changes in interest rates also puts upward pressure on interest rates, albeit temporary. Let’s take a look…

Mortgage-Backed Securities (MBS)

Hedging MBS are a perfect example. MBS are securities backed by a pool or group of individual mortgages. One of the main risks of these securities is prepayment risk. Specifically, individuals have the right to repay their mortgage without any penalties. These prepayments impact the average life of the security. Average life is a metric estimating how long the principal, on average, will be outstanding. In periods of falling interest rates, the average life will contract assuming folks will refinance their mortgage at a lower interest rate to lower their monthly payment. This is referred to as contraction risk. The opposite is also true, when rates are going higher, folks tend not refinance which will have the impact of keeping the principal outstanding for a longer period of time. This will extend the average life. Not surprisingly, this is referred to as extension risk.

Hedging Extension Risk

Since we are in a period of rising rates let’s look at an example of hedging MBS with interest rate swaps. In our example, we assume that given the rising interest rate environment, the MBS portfolio manager is concerned about extension risk. (This analysis can be used for any interest rate sensitive portfolio regardless of the prepayment assumptions made for MBS.)

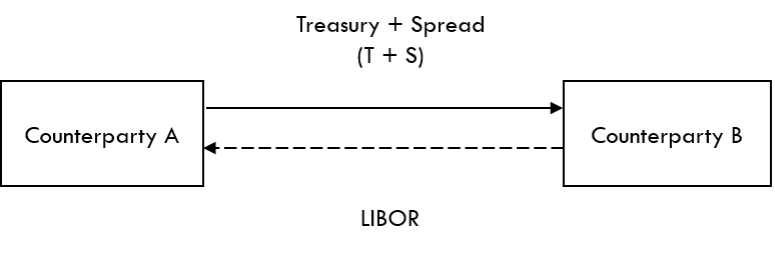

What is an Interest Rate Swap?1,2

The most common type of interest rate swap is a fixed for floating or also called a plain vanilla swap. In a plain vanilla swap one counterparty agrees to pay a fixed rate of interest while the other agrees to pay a floating rate of interest. Figure 1 shows the cash flows of a plain vanilla swap.

Figure 1

Counterparty A has agreed to pay a fixed rate of interest to counterparty B and Counterparty B has agreed to pay a floating rate of interest to counterparty A. Paying is equivalent to creating a liability or in accounting parlance, paying interest expense. Receiving is equivalent to creating an asset or in accounting parlance, it is receiving interest income. The focus here will be on paying the fixed leg.

Combining the MBS and Interest Rate Swap

To hedge the extension risk of the MBS, the owner of the MBS will pay the fixed rate in the swap. Below, Figure 2 shows this combination. The execution of the fixed leg will hedge the extension risk of the MBS, i.e., the MBS is an asset and the fixed leg of the swap is creating a liability. The floating leg is ignored for this analysis as it will generally have a maturity of 3-months and will not impact the analysis given it its very short maturity.

Figure 2

Interest Rate Swap Dealers

The owner of the MBS executed their transaction with an IRS dealer. The dealer now has to hedge their exposure since they are receiving the fixed leg or the asset created by the fixed leg. Now this is where the secondary effects of hedging start to come into play. The dealer has several choices to hedge but all result in putting additional upward pressure on interest rates. They can:

- Short 10-year Treasuries

- Short Treasury futures

- Enter into an offsetting swap

Let’s look at each alternative.

By shorting the cash security, the IRS dealer is putting downward pressure on price. Since there is an inverse relationship between price and yield, the hedge puts upward pressure on rates. Further assume the IRS dealer sold the UST to a government Treasury dealer. The government Treasury dealer will then sell their position to another dealer, who will sell to another, keeping downward pressure on prices.

Shorting Treasury futures will have a similar effect as shorting the cash treasuries. The IRS dealer shorts the futures contracts and puts upward pressure on rates, the buyer of the futures contract will sell their position and so on.

The third alternative will simply offset the IRS dealer’s position. However, they have simply transferred their risk to another IRS dealer who will have to choose between shorting the cash Treasury or the Treasury futures, thereby pressuring prices downward as well.

Conclusion

Economic fundamentals, supply chain issues and energy prices have all contributed to interest rates moving higher. However, dealers in their market making capacity hedge their exposures. This act of hedging will put downward pressure on prices/upward pressure on rates. These transactions will be executed until the buyers and sellers find a proper equilibrium! This should be taken in context as the overall trend in rates is now up.

Endnotes

1 At the time of this writing, in the United States, the markets are still converting to SOFR swaps from LIBOR based swaps. Regardless of which type of swap is being used, it does not change the concepts of hedging.

2 Swaptions can also be used for hedging MBS but that is for another day!

3 MBS return can be a nominal spread over the average life of the comparable US Treasury or an option adjusted spread (OAS). In addition, different horizon analyses can be simulated. For purposes of this blog, it is easier to think it as a T + S.