At the end of this past week, headlines on the financial news pages around the United States if not the world, alerted us all to a rare and unsettling event:

“Treasury Market Calls Time on Fed Hikes as Curve Finally Inverts” (Bloomberg, 3/22/19)

“Stocks, Bond Yields Fall Amid Anxiety Over World Economy” (The Wall Street Journal, 3/22/19)

“Two prominent warning signals from bonds.” (The Wall Street Journal, 3/24/19)

The U.S. Treasury Market is the bedrock of the U.S. bond market, and yields on U.S. Treasuries form the basis of pricing virtually all other U.S. dollar denominated bonds issued by U.S. entities such as corporations and financial institutions. The Treasury Bond Market is where the U.S. Government borrows money, and as such, is considered “risk free” from default (recent government closure notwithstanding!). Since the yields on Treasury notes and bonds are the “risk free” yield at any maturity, they become the pricing point over which an appropriate credit and liquidity spread is added to determine the yield on any other issuer, e.g., a corporate issuer or a financial institution. This is commonly referred to as Treasuries plus a Spread (T + S).

The U.S. Treasury Market “yield curve” is merely a depiction of the yields on Treasury notes and bonds at different maturities, usually shown from very short-term Treasuries (referred to as Treasury “bills” or T-bills), to longer-term maturities (referred to as Treasury “notes” and “bonds”). Although Treasury bonds are issued with maturities of 30 years, market interest is usually in the 1–10-year range. Treasury notes in this range are also watched closely as an indicator of shifts in investor sentiment about the outlook for the U.S. economy, as well as signals about Federal Reserve Bank policy regarding dampening or stimulating the U.S. economy by raising or lowering short term rates, such as the Fed Funds rate and Interest On Excess Reserves (IOER). When the Fed lowers these short-term rates, it usually indicates that they want to stimulate the economy by making it cheaper for banks and companies to borrow money. When the Fed raises short-term rates, it can indicate a variety of things, including a desire to dampen the economy, take advantage of a buoyant economy by raising rates to curb inflation, and gain sufficient room to move rates lower should the economy begin to weaken and economic stimulus is needed to resuscitate growth.

My own view is that the Fed had been raising short-term rates carefully in the Yellen years after the last recession, and the current Fed has continued, but slowed, that rise in order to maintain that dry powder for future stimulus (but without dampening growth).

On the long-end of the yield curve, different forces seem to be at work. Last Friday the Wall Street Journalreported a shift from stocks to bonds by investors who believe equity markets are weak and getting weaker, and who are shifting funds into longer-term Treasury notes and bonds. Purchasers of those bonds drive their prices up and their yields down. The Wall Street Journalarticle reported that this appears to have happened in both Germany and the United States.

“A report Friday showed factory output in the eurozone fell in March at the fastest pace in nearly six years, while a gauge of U.S. manufacturing activity slipped to its lowest level in nearly two years. The data sent bond prices rising and yields sliding, with the German 10-year bond yield dropping below zero for the first time since 2016 and the yield on the 10-year Treasury note falling to 2.459%, the lowest since January 2018.” – Stocks, Bond Yields Fall Amid Anxiety Over World Economy, WSJ, 3/22/19

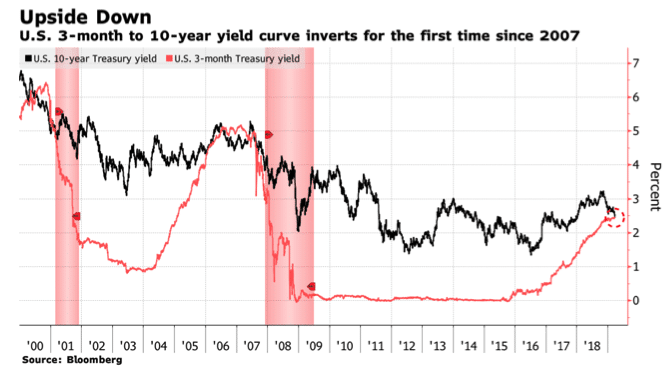

The Treasury yield curve is usually “upward sloping,” meaning that T-bill rates are normally lower than longer-term rates. (Comparing two points on the Treasury curve is often referred to as a spread or yield curve spread. More often than not, it is just called the yield curve!). However, when the yield curve inverts, and short rates are higher than long rates, it is generally interpreted as a sign that a weakening economy and/or an economic recession are anticipated in the near future. Hence, the alarm in the markets occurring from this “inverted” yield curve! As demonstrated by the chart below, the 3-month Treasury Bill is above the 10-year Treasury. This inversion has coincided with the previous two recessions.

It is interesting to note that there are two other yield curve spreads that market practitioners watch: the 2s/10s (the 10-year Treasury minus the 2-year Treasury) and the 3-month versus the 30-year Treasury (the 30-year Treasury minus the 3-month Treasury Bill). These have not yet inverted and have been excellent predictors of future recessions when they do invert. So, it may simply be a wait and see scenario!

Just as an “inverted yield curve” may signal an impending recession, other yield curve shapes may signal different stages of the economy. The dynamics of yield curves are covered in GFMI’s Yield Curve Analysis course; we welcome you to explore what is covered in this class at https://www.gfmi.com/training_courses/understanding-yield-curve-analysis/.