High fashion and high finance may have an all too apparent connection when it comes to the new season and folks with considerable means go shopping for the latest styles in trendy boutiques. Last season’s finery may well have drifted rapidly out of style and that change may take its toll on one’s liquid assets.

However, in the investment world, “style” refers to a portfolio manager’s method and strategy of investment and “style drift” refers to subtle and persistent changes in a portfolio manager’s “style.” Most large investment funds have a very well-defined methodology and style so that they can appeal to particular types of investors as well as achieve particular returns in specified market conditions which are what their investors are expecting. A change in “style” connotes a decisive change in the investment strategy of a fund to take advantage of a change in market conditions, whereas “style drift” connotes a more gradual and perhaps less deliberate change in the investment strategy of the fund. But it is a distinct change, nonetheless.

To illustrate style drift, let’s consider hedge funds since they have a wide variety of strategies involving long and short positions in different instruments, e.g., convertible bond arbitrage, equity long/short, pairs trading, equity market-neutral, and merger arbitrage. Each of these strategies is very distinct and would be expected to perform differently in different market environments. Consider a hedge fund engaging in pairs trading. This fund would seek to recognize and take advantage of trading abnormalities between two different stocks, take short-term positions when those relationships become temporarily distorted in the market, and profit when the relationship returns to normal. The change in relationship would occur over a relatively short period of time – often less than a day – and the fund might enter the trade in the morning and exit it in the afternoon, making a profit.

By contrast, an equity long/short fund would analyze intrinsic value in stocks, purchase stocks they believe will appreciate over time, and simultaneously short stocks they believe will depreciate over time. The holding period might be months or much longer until the appreciation or depreciation occurs.

Consider a situation where a pairs trader puts on a trade based on what she thought was a market aberration. When the aberration did not correct itself, she decided to keep both positions on with the expectation that one would continue to rise and the other to fall. This is a very significant example of style drift. Style drift can entail unpleasant surprises for investors and hedge fund investors are usually very conscious of style drift.

Recently, the Woodford Equity Income Fund provided a real case of documented style drift, outlined in the MSCI newsletter “Lessons from Woodford: Shutting the barn door after the horses have bolted”, 14 June 2019 (“Lessons from Woodward”). Let’s look at the fund in question, the LF Woodford Equity Income Fund, inception 2 June 2014.

According to the LF Woodford Equity Income Fund Fact Sheet as of 30 April 2019, the fund’s benchmark index is the FTSE All Share index, IA UK All Companies sector, the fund has UCITS (UK) status, with daily pricing frequency, and a Sterling 4.33 billion fund size. Investors in the fund have the right to buy or redeem their shares on a daily basis. The fund’s Investment Objective is “To provide a reasonable level of income together with capital growth. This will be achieved by investing primarily in UK listed companies.” Under the risks section of the Fact Sheet, the final risk is described: “The fund may invest in unquoted securities, which may be less liquid and more difficult to value, because they are generally not publicly traded – the lack of an open market may also make it more difficult to establish fair value.”

On its face, these seem to be somewhat vague and contradictory objectives without a clear statement of a target proportion of actively quoted vs. unquoted securities. In other words, the strategy and investment style of the fund is ambiguous and left open to the discretion of the fund manager on an ad hoc basis. This is a perfect recipe for “style drift” as market conditions change.

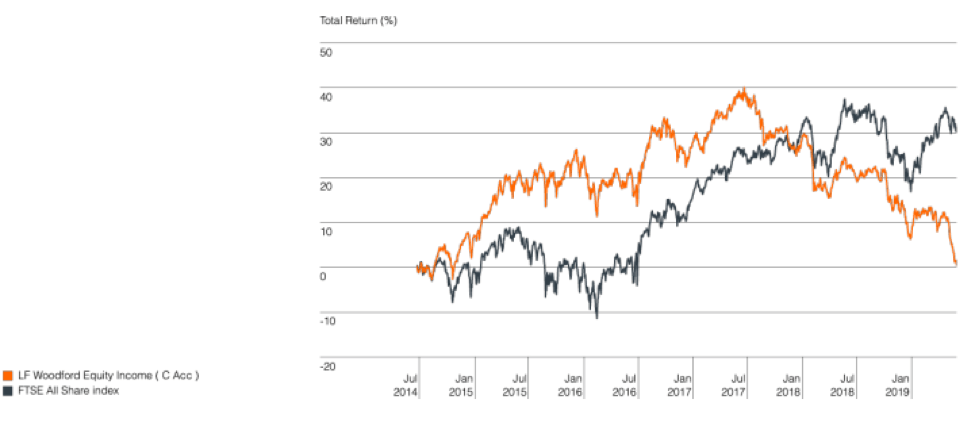

The Fact Sheet goes on to show us the following performance. As is evident from the chart, the fund handsomely outperformed its benchmark index until the second half of 2017 where it turned negative relative to the benchmark around January 2018.

Performance since launch – Source: Financial Express, Woodford

Source: LF Woodford Equity Income Fund Fact Sheet as of 30 April 2019

Ultimately, the fund suspended withdrawals on June 3, 2019.

According to the MSCI analysis, the reason for suspension appears to be that the fund persistently sold liquid securities in order to meet redemption demands from investors, and that this persistent sale of liquid securities persistently increased the proportion of the fund held in illiquid securities. “Six months before the Woodford Equity Income Fund suspended withdrawals on June 3, the level of illiquid securities stood close to 80% of assets, and the fund had drifted away from its investment objective ‘to provide reasonable level of income together with capital growth.’” (“Lessons from Woodward”) The reason for the fund’s demise appears to have been style drift.

In a future blog, we will consider ways in which investors can monitor and react more quickly to style drift.