The Roaring ‘20s are here! The world of finance looks wonderful – the Dow Jones Industrial Average is at record highs, inflation and interest rates are low, unemployment is at an all-time low, and trade tensions have eased. What could go wrong?

Plenty.

The Bull Market started in March 2009 and is the longest running Bull Market in the history of the United States. That being said, the financial world as we know it today cannot last forever. The Piper will be coming, yet no one knows when. My concern centers on the debt markets and the extended use of leverage with little or no covenants to protect the investor.

When the leveraged buyout boom began in the 1980s, large banks provided the vast majority of the debt. Bankers who had rigorous credit training (think financial statement analysis, ratio analysis, and forecasting) were very careful to structure their deals with tight covenants to ensure timely payback from the borrower. That lasted until the Great Recession. After the Great Recession, banks were either unable or unwilling to provide the majority of the debt for an LBO as they had to clean up their balance sheets and heed to the regulators’ new restrictions.

Cov-Lite Loans

But while the banks’ interest waned for LBOs, other providers of debt (such as hedge funds, institutional investors, etc.) were eager to put their money to work. With interest rates near zero – or in many countries negative – investors are seeking yield. What better place than the debt markets? With so much liquidity in the markets and a limited supply of deals, borrowers have been able to negotiate much more favorable terms and conditions. Born was the covenant lite (Cov-Lite) loan.

Traditional bank loans have covenants in order to provide a level of certainty to the investor by restricting or requiring certain actions of the borrower. They include maintenance and incurrence covenants. Maintenance covenants are tested regularly (e.g., every 3 months) and can include tests such as minimum net worth, debt/EBITDA not to exceed X, maximum capital expenditures of X, and minimum interest coverage of X. Incurrence covenants are tested for specific events such as incurring additional indebtedness, paying dividends, and acquiring new businesses.

When a borrower begins to have financial difficulty, the breach of financial covenants gives the lender a warning sign and allows the lender to either amend the covenant for a period of time or restructure the deal to allow the borrower some much needed breathing room. Cov-Lite loans essentially ditch the maintenance covenants, leaving the lender with little recourse when something goes amiss with the borrower.

Documentation

Another fallout of Cov-Lite loans is the documentation. Be aware of how EBITDA is defined and the various add-backs that often inflate EBITDA into the stratosphere. Look at some of the add-backs that are very real costs, yet included in EBITDA. For example:

- EBITDAC – change in acquisition costs

- EBITDAO – option expenses

- EBITDAP – pension expenses

- EBITDAR – lease/rental expenses

- EBITDARE – losses, gains, and other adjustments on real estate

- EBITDAS – stock based compensation

- And the best one: Community-adjusted EBITDA – including marketing, development, and administrative costs (employed at WeWork)

Documentation can also allow for additional indebtedness, transfer of assets to unrestricted subsidiaries, and unrestricted asset sales – all to the detriment of the lenders.

Decline of Credit Quality

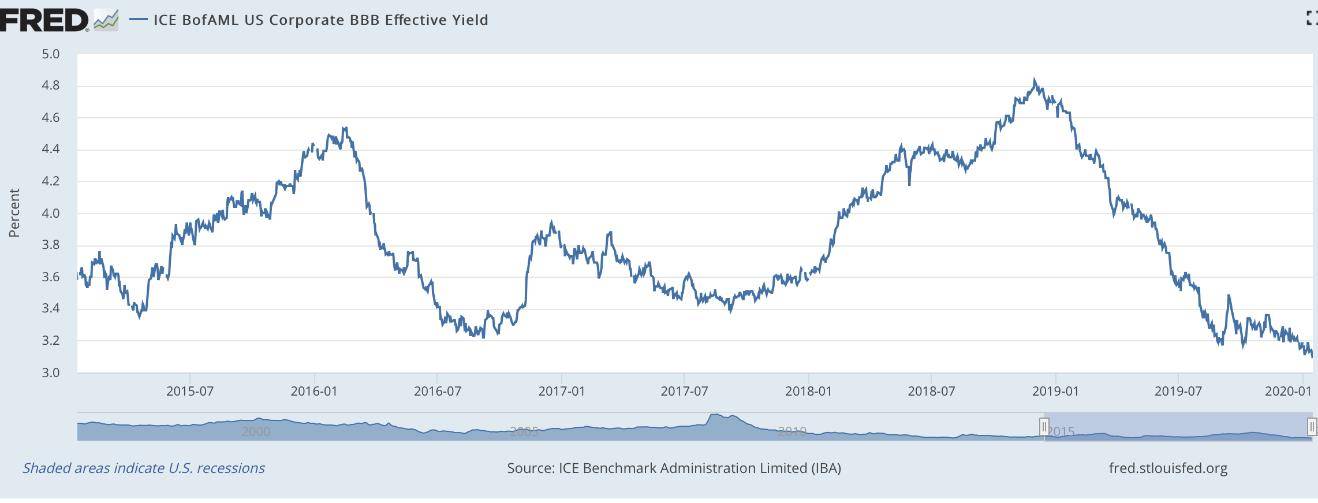

As the market continues to enjoy leverage, credit quality has declined. Below is a chart of BBB yields through January 2020. BBB rated debt makes up close to 50% of all investment grade debt, yet pays rather paltry yields.

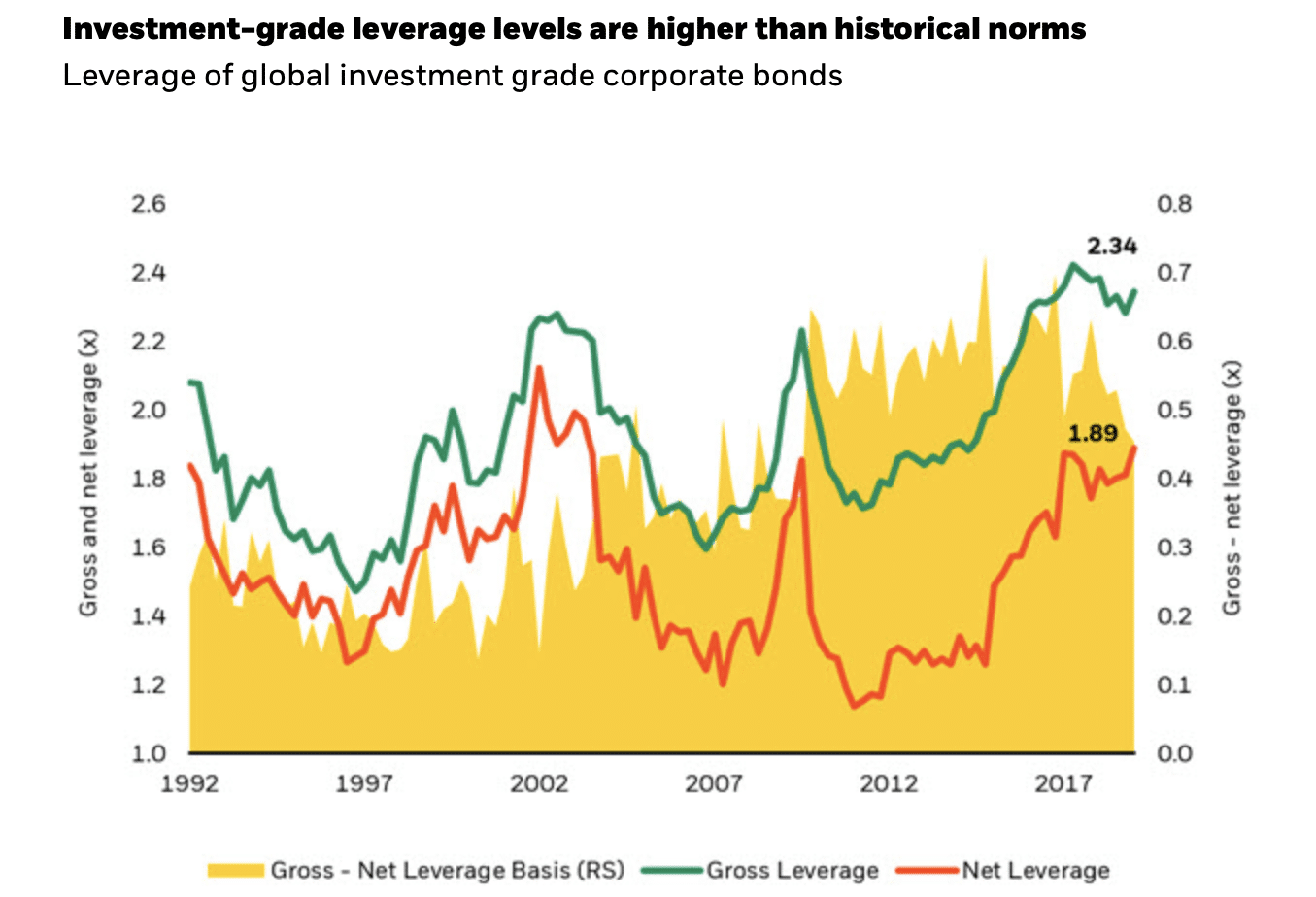

Another discouraging statistic is the actual amount of leverage as seen in the following graphic:

Gross leverage is calculated as

| Total Deb

|

| 12-month EBITDA |

Net leverage is calculated as:

| Total Debt less Cash and Cash Equivalents

|

| 12-month EBITDA |

A shrinking basis between gross and net leverage is usually a sign that investment-grade balance sheets are holding less cash. Higher measures of leverage typically indicate greater issuer risk.

Cov-Lite loans now make up approximately 80% of all leveraged deals. Market participants seem to agree that credit losses will be greater for Cov-Lite loans when the credit cycle turns. Just how much? No one knows at this juncture. S&P Global Market Intelligence found the following:

“S&P’s LossStats, and LCD, conducted analysis on recoveries of cov-lite loans that defaulted before the 2008-09 financial crisis, versus those that were structured and defaulted after the crisis. The later-vintage group of cov-lite loans saw an average discounted recovery of 56%, compared to a 78% average recovery on the earlier deals.”

Source: S&P Global Market Intelligence: Leveraged Loans: Another New Record for Covenant-Lite, August 9, 2018

What Next?

Recently I was teaching a credit analysis course and mentioned to the client that Cov-Lite loans can be quite risky in the event of a downturn. He responded, “If we don’t do these deals, we won’t book any business and you and I will both be out of jobs.” Possibly true, but someone will have to be around to clean up the mess.

We all know that there will be a downturn in the market. It is not a question of if, but when. Many lenders and regulators stand the risk of being surprised by the lack of protection they currently have with their Cov-Lite loans.

About the Author: Julie Barnum

Julie is also a Director and Chief Credit Officer of Yavapai Regional Capital, a regional infrastructure merchant bank which specializes in advisory and management work for public private partnerships in the southwestern United States.

Prior to starting her own consulting business, Julie was with Pearson plc for four years, as the Global Director of Credit for the FT Knowledge/NY Institute of Finance training arm. Here, she headed up all Credit and Corporate Finance related learning programs – creating and delivering custom curriculums. Her case study materials were used for Valuations, Capital Structuring, Projections, Strategy, and Covenant Setting. Later, as the Managing Director for NYIF, her responsibilities included the public course schedule and oversight of Accounting, CFA Exam Prep, Credit Risk, Corporate Finance, Fixed Income, Portfolio Analysis, Technical Analysis and Wealth Management courses.

Prior to Pearson, Julie worked for over 15 years with various divisions of Paribas in Los Angeles, Paris, and New York. For example, she served as a Senior Credit Officer in the Risk Management Division, where she approved all new and existing media, telecom, and entertainment related loans in North and South America, with structures ranging from negative cash-flow loans with equity kickers to large syndicated credits. She approved all corporate loans in the Southwest region with emphasis on leveraged transactions in corporate roll-ups, waste management, and leveraged aircraft finance. As the Head of International Training for the Corporate Banking Division, Julie designed, implemented, and managed Credit Training, covering 60 countries and 2,000 employees, conducted global needs analysis, leading to creation of Paribas’ first in-house worldwide Credit Training Program, and delivered one-week entry level credit programs in China and the Mid-East.

Copyright © 2020 by Global Financial Markets Institute, Inc.

23 Maytime Court

Jericho, NY 11753

+1 516 935 0923

www.GFMI.com

Download article