Settlement risk has been part of the capital markets since its inception. Blockchain is the new kid on the block. Can Blockchain, sometimes referred to as Distributed Ledger Technology (DLT), help mitigate settlement risk or is it all a pipe dream?

Speaking of pipes, the industry infrastructure (sometimes referred to as the “plumbing”) includes many different “pipes” for the flow of trading and settlement activity, of which settlement is one. This quick article defines settlement risk, examines ways to mitigate it, and discusses the potential for applying Blockchain during the settlement process.

Settlement Risk

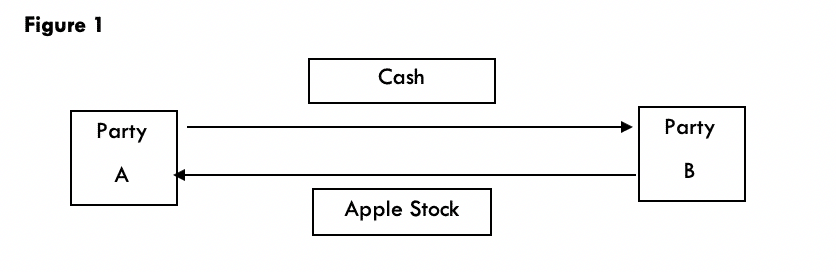

In any capital markets transaction, the buyer pays the seller for the delivery of the securities or other asset type, on the settlement date of the trade. One party must pay the other party for the security, commodity, or currency they are purchasing. For example, assume Party A buys 100 shares of Apple stock from Party B. If all goes right, the cash and securities are exchanged and both parties walk away happy i.e. the financial obligations agreed to at the time of the trade are fulfilled. This is shown in Figure 1:

Figure 1

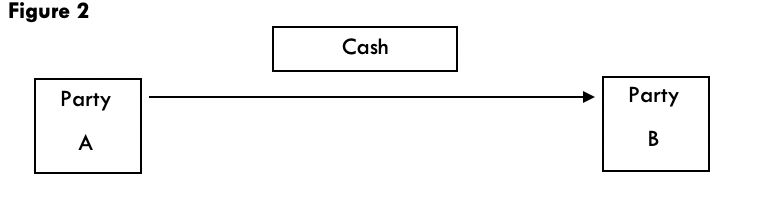

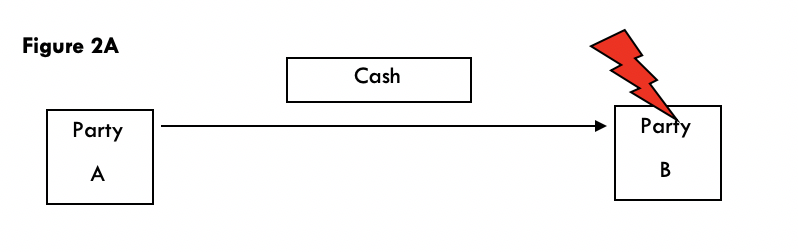

Now assume that Party A pays Party B. After A pays B for the expected delivery of the shares of Apple, Party B goes bankrupt. Party B never delivers the stock but has received the cash payment. This is shown in Figures 2 and 2A. Party A will most likely have to go to bankruptcy court to get their money. That could take years and they may only get a fraction of their money or possibly nothing at all.

Figure 2

Figure 2A

The foreign exchange markets have a perfect example of settlement risk. In the mid-1970s, German regulators walked into Herstatt Bank in the late afternoon and closed them down. Market participants that transacted foreign exchange trades with Herstatt continued to remit Deutsche Marks expecting USD in return. The dollars never showed up! Hence in the FX markets, settlement risk is often referred to as Herstatt risk.1

Managing Settlement Risk

There are several ways to mitigate settlement risk:

- Delivery versus Payment (DvP)

- Settle the transaction through a third party such as a clearinghouse

- Payment versus Payment (PvP)

Delivery Versus Payment (DvP)

This concept is fairly straightforward. In our first example (Figure 1), Party B would have to deliver the stock (security) first and then and only then would Party A release the cash.

The settlement of the trade will require a simultaneous exchange of assets. Party A receives the securities at the same time Party B is receiving the cash.

Clearinghouses

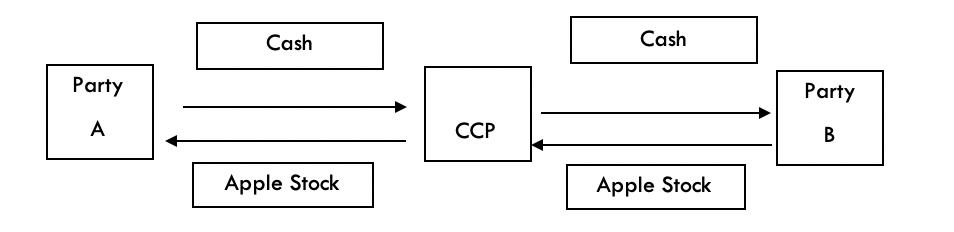

A clearinghouse, sometimes referred to as a Central Counterparty (CCP), is an industry-wide centralized processing system established in financial markets. In some markets, a clearing house supports the clearing of securities, while another may support the clearing of derivatives, and in others they support both. When a trade is cleared, the CCP inserts themselves between the two parties of the trade, which is often described as “becomes the buyer to every seller, and the seller to every buyer.” To be clear (no pun intended), Party A and B initially agree to the terms of the transaction but then assign or “novate” the legal ownership of the trade to the CCP. Figure 1 above is settlement without the CCP. Figure 3 is with a CCP:

Figure 3

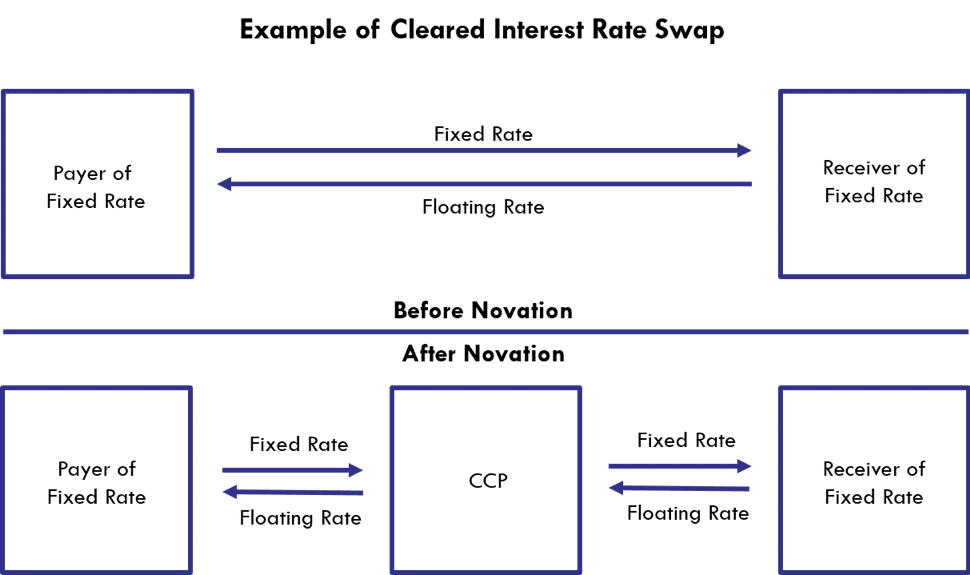

Figure 4 shows before and after novation with an interest rate swap. By introducing the CCP, the settlement risk is now shifted to the CCP. The CCP is made up of clearing members who must provide margin or collateral to the clearing house. This collateral will serve as the financial safeguard or resources for the clearing house and its members in the event that a clearing member goes into default. For more detailed information on Central Counterparties see our article “Understanding Central Counterparties” (https://www.gfmi.com/insights/articles/).

Figure 4

Payment versus payment (PvP)

In a foreign exchange transaction one currency is exchanged for another currency. CLS Group was created to reduce settlement risk. An FX transaction can either settle spot (which generally refers to trade date plus 1 or 2 business days, depending on the currency) or forward (which implies that it settles on some date after the spot date).

Both parties send their payment instructions/details to CLS. CLS then confirms the details, runs various risk management steps, and then simultaneously settles both currencies in the transaction on the agreed to settlement date.

Enter Blockchain?

Blockchain2has promised to transform the financial markets from operations, trade finance, insurance, payment systems, rehypothecation and compliance, to creating world peace (not really, but sometimes it sure feels that way with everyone saying how great it is!!). Analogies have been made to the Internet changing media, with Blockchain changing financial services. Financial institutions have been experimenting with blockchain and spending a fair bit of money on it. To be sure, according to the BIS, Blockchain has “… the potential to disrupt payment, clearing, settlement and related activities.”3

However, there are still hurdles, specifically legal and regulatory, as well as the test of time. Significant resources would be required to replace the legacy systems and “pipes.” In their January 2018 paper, “Modernizing the U.S. Equity Markets Post-Trade Infrastructure,” the DTCC4stated “In the equity cash market, the promise of DLT must first overcome significant hurdles with regard to speed and scale. Today, an average of more than 50 million trades are processed daily — which can, and has, spiked on occasion to over 120 million and as many as 25,000 transactions per second during peak processing. Any technology implemented would need to meet the industry standard of handling at least two-to-three times the current market volume peak … In addition, the current landscape of multiple DLT providers raises issues of fragmentation and interoperability that would need to be addressed because distributing or bifurcating clearing would eliminate the significant netting and risk management benefits experienced today.”

It appears that Blockchain may lead us to the promised land — but not quite yet!

Footnotes

1For a summary and interesting take on this event go to https://bankunderground.co.uk/2015/06/24/boe-archives-reveal-little-known-lesson-from-the-1974-failure-of-herstatt-bank/

2See GFMI’s article “Blockchain – Where We Have Been & Where We Are Going” https://www.gfmi.com/insights/articles/

3Distributed ledger technology in payment, clearing and settlement – An analytical framework, BIS Committee on Payments and Market Infrastructure, February 2017

4Modernizing the U.S. Equity Markets Post-Trade Infrastructure – A White Paper to the Industry, DTCC, January 2018

About the Author: Kenneth Kapner

He has been a Risk Management Advisor to a Mutual Fund’s Board of Trustees and has served as an Expert Witness using knowledge of derivatives, trading and risk management.

Prior to starting GFMI in 1998, Ken spent 14 years with the HSBC (Hong Kong and Shanghai Banking Corporation) Group in their Treasury and Capital markets area where he traded a variety of instruments including interest rate derivatives, spot and forward foreign exchange, money markets; managed the balance sheet; sat on the Asset Liability Committee; and was responsible for the overall Treasury activities of the bank. He later headed up HSBC’s Global Treasury and Capital Markets Product training for two years in Hong Kong. Specifically, his responsibilities included developing new courses and delivering courses to traders, support staff and relationship managers. In New York, he established a training department for the firms’ Securities Division where he was in charge of the MBA Associates Program, continuing education and Section 20 license.

He has co-authored/co-edited seven books on derivatives including The Swaps Handbook and Understanding Swaps.

Copyright © 2018 by Global Financial Markets Institute, Inc.

Download article