I asked one of my friends what they thought SPAC could stand for. As it is the holiday season, she replied, “Send Presents at Christmas?” Nice try, but no cigar. SPACs, or Special Purpose Acquisition Companies, have been around for years, but recently have garnered much more attention due to the pandemic induced influx of new retail investors and traders.

What are SPACs and How Do They Work?

SPACs offer a less cumbersome and less expensive way for companies to go public. They are created by an equity sponsor ranging from a private equity shop to celebrities (e.g., Shaq O’Neal, Stephen Curry, Serena Williams, Alex Rodriguez, and Colin Kaepernick, to name a few). Funds are raised in the public equity markets; the SPAC trades on the exchange with an eye to find a target company with which to merge. The “blank check” company has up two years to find a target. Once the target is found, the SPAC does a reverse merger and takes on the identity and ticker symbol of the target company.

Let’s dig into some of the weeds of this process. The SPAC process is a follows:

A financial sponsor (think private equity, hedge funds, venture capital, and even celebrities) form the SPAC. The sponsors get an equity stake of 20%.

The SPAC raises capital via an IPO. Following the IPO, SPAC proceeds are placed in an escrow account and invested in highly liquid securities, such as U.S. Treasuries. The SPAC normally has two years to complete an acquisition. If the SPAC does not make an acquisition within the timeframe, the SPAC is dissolved and the funds are returned to the investors. SPAC shares are normally priced at $10 per unit and may have a warrant attached.

The SPAC searches for a suitable private company. Some SPACs are specific about the industries they will invest in, while others are open-ended.

The equity sponsors negotiate with the target company and seek approval from the SPAC shareholders. Under SPAC rules, a company bought by the SPAC must have a fair market value of at least 80% of the funds deposited with the SPAC at its founding.

The target acquisition closes by merging into the SPAC, and the target company becomes a publicly traded entity. A Super 8-K must be filed with the SEC. Furthermore, the sponsor’s founders’ shares and warrants are locked up for a specified period (the “lock-up period”) starting from the date of the Super 8-K filing.

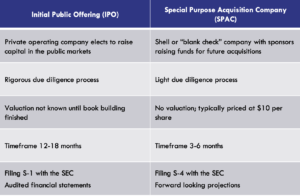

See below for the broad differences between an IPO and a SPAC:

Why Have SPACs Become So Popular?

There is an enormous amount of private capital sitting on the sidelines, waiting for a return to normalcy. It is estimated that there is over $165 billion of SPAC raised dry powder waiting to find a target. That translates into between $700 billion and $1 trillion of buying power.1 That is an enormous amount of buying power!

SEC

The SEC has been reviewing SPACs and addressing both regulatory and investor protection issues. The Investor Advisory Committee2 has offered the following preliminary recommendations for consideration:

Disclosure

Disclosure of the role of the SPAC sponsor, including disclosure of the sponsor’s appropriateness, expertise and capital contributions, as well as an overview of any potential conflicts of interest on the part of the sponsor

Plain English disclosure in the SPAC registration statement (beyond mere financial footnotes) around the economics of the various participants in a SPAC process, including the founder shares paid and their impact on dilution

Disclosure that includes a clear description (with diagrams or charts as appropriate) in the SPAC registration statement of the mechanics and timeline of the SPAC process

Disclosure in the SPAC registration statement regarding the opportunity set and target company areas of focus, including a clearer description of the boundaries of the search area and attributes of acceptable and unacceptable companies

Disclosure regarding the competitive pressure and risks involved in finding appropriate targets and reaching market acceptable prices for these companies

Disclosure of the acceptable range of terms under which any additional funding might be sought at the time of the acquisition

Disclosure regarding the manner in which the sponsor plans the assess the capability of potential targets

Disclosure of the minimum pre-de-SPAC diligence the sponsor will commit to regarding accounting practices used by the target company, including audit history, use of GAAP and non-GAAP pro forma numbers

Risks

According to FINRA3, SPACs have certain risks, which must be disclosed to investors and which must be the subject of the broker-dealer’s suitability analysis. For example, SPAC IPOs present the following two risks:

The risk that the SPAC managers are unqualified or incompetent, a risk made more pronounced by lack of any operating history or past performance.

The risk that no acquisition will occur and the SPAC will be liquidated. Investors may be able to sell their SPAC units in the secondary market, but they bear the opportunity cost of waiting for a determination about whether an acquisition will occur or sell in the secondary market before the outcome is determined.

An excellent research paper entitled A Sober Look at SPACs4 notes the following:

“The sponsor’s essentially free shares and the IPO investors’ free warrants dilute the value of the SPAC’s shares, and the underwriting fees further deplete the SPAC’s cash. SPAC redemptions then amplify the effects of dilution and dissipation of cash on a per-share basis. . . . As a result of these costs, by the time the SPAC merges with a target company, it has far less net cash per share than the $10.00 attributed to them in the SPAC’s merger. We find that the median SPAC delivers only $5.70 per share in net cash in its merger, which means a total of $4.10 per share has been extracted by the sponsor, the IPO investors, the underwriter, and various advisors.” (Note: The remaining $0.20 per share is for fees.)

Wow!

In summary, SPACs have their place on this earth, but one should always do their own due diligence and find out the experience of the sponsors and their experience within the industry.

Happy Holidays and, oh yeah, send presents at Christmas!

2 Recommendations of the Investor as Purchaser and Investor as Owner Subcommittees of the SEC Investor Advisory Committee regarding Special Purpose Acquisition Companies – draft as of August 25, 2021

3 FINRA Regulatory Notice 08-54 “Guidance on Special Acquisition Companies”

With an extensive professional career in the credit markets, and many years in the financial instruction field, Julie Barnum brings a unique blend of knowledge and know-how to our clients. Currently, Julie is President of her own consulting firm for large multinational corporations, government regulators and financial institutions. Her assignments cover the globe: China, Europe, Russia, Australia, and the United States.

Julie is also a Director and Chief Credit Officer of Yavapai Regional Capital, a regional infrastructure merchant bank which specializes in advisory and management work for public private partnerships in the southwestern United States.

Prior to starting her own consulting business, Julie was with Pearson plc for four years, as the Global Director of Credit for the FT Knowledge/NY Institute of Finance training arm. Here, she headed up all Credit and Corporate Finance related learning programs – creating and delivering custom curriculums. Her case study materials were used for Valuations, Capital Structuring, Projections, Strategy, and Covenant Setting. Later, as the Managing Director for NYIF, her responsibilities included the public course schedule and oversight of Accounting, CFA Exam Prep, Credit Risk, Corporate Finance, Fixed Income, Portfolio Analysis, Technical Analysis and Wealth Management courses.

Prior to Pearson, Julie worked for over 15 years with various divisions of Paribas in Los Angeles, Paris, and New York. For example, she served as a Senior Credit Officer in the Risk Management Division, where she approved all new and existing media, telecom, and entertainment related loans in North and South America, with structures ranging from negative cash-flow loans with equity kickers to large syndicated credits. She approved all corporate loans in the Southwest region with emphasis on leveraged transactions in corporate roll-ups, waste management, and leveraged aircraft finance. As the Head of International Training for the Corporate Banking Division, Julie designed, implemented, and managed Credit Training, covering 60 countries and 2,000 employees, conducted global needs analysis, leading to creation of Paribas’ first in-house worldwide Credit Training Program, and delivered one-week entry level credit programs in China and the Mid-East.