The rock band YES has a song called “Perpetual Change.” Capital markets resemble the title of the song as they are known for innovation and continually adapting to market changes. (And how apropos to have an adjective in our eNews article and a rock and roll song!) Cryptocurrencies and their derivatives are perfect examples of innovations. Futures have been around for over 150 years and the original swap – a currency swap between IBM and the World Bank – was transacted in1981. Perpetual swaps were originated in 20161and are neophytes, compared to these “ancient” derivatives! Yet, Binance, a Crypto exchange, has approximately 100 perpetual contracts listed on their exchange.

My previous article explored the CME cryptocurrency futures contract,2 which is considered more of a traditional futures contract given the fixed expiration dates. This article will explain perpetual contracts and look at their differences compared to futures with fixed expirations.

Perpetual Contracts

As pointed out in the first article, crypto derivatives now make up the majority of cryptocurrency volume as presented in the following chart:

Source: CryptoCompare Exchange Review February 2022

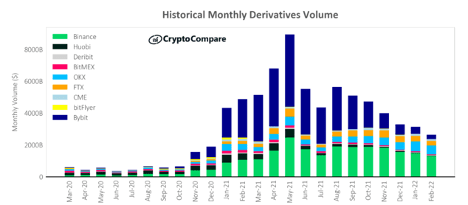

The following chart shows the volume for derivatives at different exchanges/platforms:

Source: CryptoCompare Exchange Review February 2022

As can be seen, there are many different exchanges that offer perpetual contracts (except the CME). Herein lies the challenge. There are no conventions when it comes to contract specifications. Even the contract itself may be referred to as a perpetual futures or a perpetual swaps contract! For example, Binance refers to them as perpetual futures and BitMex refers to them as perpetual swaps. I will approach the challenge from a more generic view by describing some of the differences from traditional futures contracts, such as the CME contracts.

What are Perpetual Contracts?

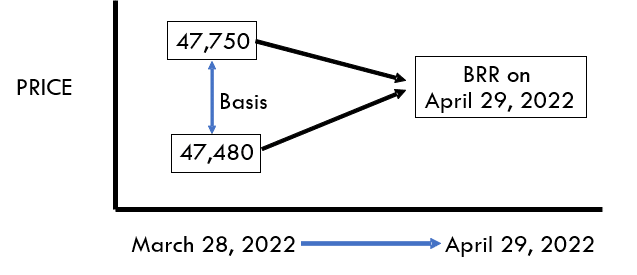

As the name implies, the contract is perpetual (I know, very profound!); that is, there is no maturity date. Recall that a futures contract with a fixed maturity will converge to the underlying cash/spot price on the maturity date as per below:

The BRR is the CME’s Bitcoin Reference Rate.3 Without a fixed maturity date, the perpetual contract requires a mechanism to ensure it closely correlates to the underlying spot/cash price.

The Funding Rate

This mechanism is known as the funding rate and has been built into the contract specifications. The concept is straight forward (no pun intended). When the perpetual contract is above the spot/cash price, the long pays the short a fee known as a funding rate. In this case, the funding is referred to as “positive.” When the price of the perpetual is below the spot/cash price of the underlying, the short pays the funding rate to the long and is referred to as “negative.” This should keep the prices closely aligned. The calculation of the funding rate is not consistent across exchanges.4

A few points here:

The underlying or spot/cash price is commonly referred to as an “index price” and is made up of spot prices from different exchanges.

The funding rate is a function of:

the underlying/index price

the perpetual price (the difference in the index price and the perpetual price is the basis, but it appears a vast majority of research, with respect to perpetuals, do not call it basis – which is a bit perplexing)

an interest rate usually determined by the exchange

a premium

The smaller the basis, the smaller the funding rate. The greater the basis, the higher the funding rate.

The timing of the funding can be calculated in any number of ways, but is often every eight hours!

If you are not long or short at the exact time of the funding, there is no fee to pay or receive.

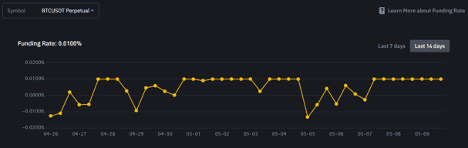

The above is not overly intuitive but here are the historical funding rates during the “funding period,” which in this case is 8 hours (from April 26 – May 9, 2022) from Binance:

As a generic example, assume a trader has a position with a notional value of $38,000 and the funding rate is 0.01%. The fee is then $38,000 x .0001 = $3.80. If the funding period is 8 hours, then the $3.80 is paid at that point in time. It is not a huge leap to see that this can quickly add up! It is also clear from the above chart that the funding rate can switch between being positive and negative.

Leverage and Auto-Liquidations

Finally, leverage can be up to 125%, and the amount of leverage, you won’t be surprised by this, depends on the exchange.

Here are some examples of leverage:

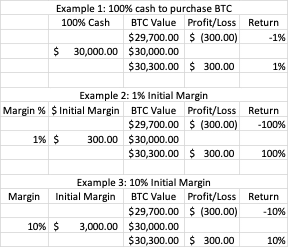

Example 1 in the table below assumes that 100% cash is used to purchase BTC/USD.

Example 2 shows a 1% initial margin which is 100x leverage.

Example 3 shows 10% initial margin which is 10x leverage. Leverage is a double-edged sword as the following table illustrates. The table assumes BTC was purchased at $30,000.

Auto-liquidation refers to a position being automatically liquidated by the exchange. The auto-liquidation is based on the size of the position, the amount of margin in the account and the exchange’s maintenance margin requirements. For example, let’s assume the initial and maintenance margin are the same. Using the 10% initial margin in the above table, and further assuming a long position was initiated at $30,000, the exchange may auto-liquidate the position at $27,500 prior to the price breaking through the $27,000. If this auto-liquidation works properly, then there is still $500 in the margin account.

This auto-liquidation is one of the first lines of defense for the exchange against default as it automatically protects the exchange from losses. However, given the volatility of cryptocurrencies, it is possible for the price to blow right through the auto-liquidation price. The exchanges have set up an insurance fund which is established for instances where there is no margin left in an account and the auto-liquidation feature didn’t work in time!

Conclusion

Perpetual contracts are very similar in nature to futures with fixed maturities with the biggest difference being its perpetual feature. To keep the perpetual contract close to the index price a mechanism known as the funding rate is employed to ensure the perpetual contract closely tracks the spot index. Leverage can be over 100x and auto-liquidation is a feature not found in traditional contracts. Nevertheless, these perpetual contracts can be used for speculating, hedging, and for the more traditional basis trade.

References

1 According to BitMEX, they introduced the Perpetual Swap Contract in 2016.

2 The article can be found at https://www.gfmi.com/articles/cryptocurrency-derivatives-chicago-mercantile-exchange-cryptocurrency-futures/

3 For more information see the above referenced article

4 For a more in depth look at the funding rate and how different exchanges calculate it go to: https://coinmetrics.io/derivatives-disparities-surveying-the-bitcoin-perpetual-swaps-market/

About the Author: Kenneth Kapner

Ken Kapner, CEO and President, started Global Financial Markets Institute, Inc. (GFMI) a NASBA certified financial learning and consulting boutique, in 1998. For over two decades, Ken has designed, developed and delivered custom instructor led training courses for a variety of clients including most Federal Government Regulators, Asset Managers, Banks, and Insurance Companies as well as a variety of support functions for these clients. Ken is well-versed in most aspects of the Capital Markets. His specific areas of expertise include derivative products, risk management, foreign exchange, fixed income, structured finance, and portfolio management. He has been a Risk Management Advisor to a Mutual Fund’s Board of Trustees and has served as an Expert Witness using knowledge of derivatives, trading and risk management.

Prior to starting GFMI in 1998, Ken spent 14 years with the HSBC (Hong Kong and Shanghai Banking Corporation) Group in their Treasury and Capital markets area where he traded a variety of instruments including interest rate derivatives, spot and forward foreign exchange, money markets; managed the balance sheet; sat on the Asset Liability Committee; and was responsible for the overall Treasury activities of the bank. He later headed up HSBC’s Global Treasury and Capital Markets Product training for two years in Hong Kong. Specifically, his responsibilities included developing new courses and delivering courses to traders, support staff and relationship managers. In New York, he established a training department for the firms’ Securities Division where he was in charge of the MBA Associates Program, continuing education and Section 20 license.

He has co-authored/co-edited seven books on derivatives including The Swaps Handbook and Understanding Swaps.

Publications and Articles

Articles

2022 CME Cryptocurrency Futures

2021 The Federal Reserve’s Tools to Manage Monetary Policy and Everything You Wanted to Know About Inflation but Were Afraid to Ask

2020 Modern Monetary Theory: The Federal Reserve, Inflation, and the US Dollar

2019 3-Month SOFR Futures and LIBOR Schmibor: What’s Next? SOFR Part I and Part II

2018 VIX, Volatilities, and Exchange Traded Products and Settlement Risk and Blockchain

2017 Electronic Trading and Flash Crashes – Part I and Part II

2016 The Long and Short of IT: An Overview of XVA, The Long and Short of IT: An Overview STACR and CAS, The Federal Reserve Tolls: Past and Present, The Perfect Storm: October 2008, and Interest Rate Swap Futures: An Introduction

2014 Risk Reversals

2002 Futures Magazine, Doing Your Homework on Individual Equity Futures (Co-written with Robert McDonough)

Blog

Ken also edits and writes for the GFMI Blog.

Books

1996 Como Entender Los Swaps (co-author: John Marshall), published by CECSA (a Mexican publishing firm). This is a translated edition of our book Understanding Swaps, but with adaptations to fit the Mexican markets. (289 pages)

1993 The Swaps Market: 2nd edition, Kolb Publishing, 288 pages (co-author: John Marshall, copyright 1993). This book is directed to the graduate business student.

1993 Understanding Swaps, John Wiley & Sons, 270 pages (co-author John Marshall, copyright 1993). This book is directed to the practitioner market and is published as part of Wiley’s Finance Series.

1993 1993-94 Supplement to the Swaps Handbook, New York Institute of Finance, a Simon & Schuster Company, 494 pages, (co-authors John Marshall and Ellen Lonergan, copyright 1993). This book is directed to a practitioner audience and is a supplement to The Swaps Handbook. My role was largely that of editor.

1991 1991-92 Supplement to The Swaps Handbook, New York Institute of Finance (Simon & Schuster Professional Information Group), 300+ pages (co-author: John Marshall copyright 1992). This book is directed to a professional practitioner audience and is an annual supplement to The Swaps Handbook.

1990 The Swaps Handbook: Swaps and Related Risk Management Instruments, New York: New York Institute of Finance, a Simon & Schuster Company, 543 pages. (co-author: John Marshall). This book is directed to derivative product professionals.

1988 Understanding Swap Finance, Cincinnati: South Western publishing Company, 155 pages. (co-author John Marshall, copyright 1990). This was the first academic text published on the swaps markets.

Affiliations

International Association of Financial Engineers Board of Advisors – 1994 – 2010