Cryptocurrency derivatives now make up the majority of the cryptocurrency market. I will be writing a series of articles/blogs on the spot and derivatives markets. This first article will address the cryptocurrency futures markets and, in particular, will give an overview of the Chicago Mercantile Exchange (CME) contracts.

Cryptocurrency futures have various features:

Regulated vs. unregulated

Fixed expirations vs. perpetual

Futures contracts are traditionally structured with fixed expirations

Perpetual structure is the “new kid on the block”

Inverse futures contracts, where the value of the contract moves inversely to the direction of the price

There are no other asset classes in futures markets that offer the perpetual structure as well as the inverse feature. That being said, cryptocurrency futures achieve the same economic objectives as other future contracts such as energy, agricultural and financial contracts. This article examines those economic objectives, specifically speculation and hedging. Arbitrage, another strategy used in futures, will be discussed in a later blog/article. There are, however, differences in the underlying securities/instruments, let alone the volatility of spot Bitcoin. Energy, agricultural, and financial spot/cash markets do not trade 24/7 whereas the spot/cash market in crypto currencies does trade 24/7. How are these differences addressed in the futures contract specifications?

To help answer this question, we begin by examining the contract specifications and then discusses the economic objectives. CME1 contracts fall into the category of traditional futures contracts (i.e., fixed expirations) and are regulated by the Commodities Futures Trade Commission (CFTC). (The perpetual futures contract will also be part of the above-mentioned blogs/articles.) Please note that this article assumes that the reader has a fundamental understanding on the mechanics of futures contracts.

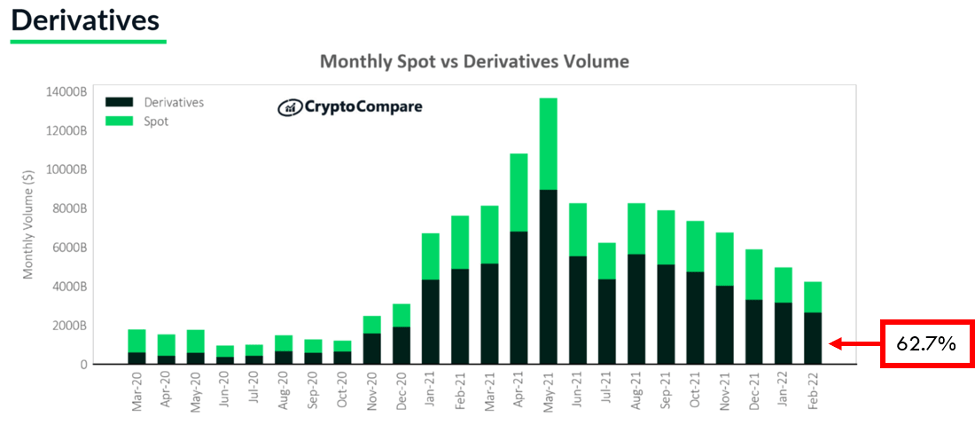

As stated in the first sentence, the cryptocurrency derivatives market now makes up the majority of the market. Specifically, as of February 2022, derivatives make up 62.7% of the cryptocurrency market!

Source: CryptoCompare Exchange Review February 2022

Bitcoin futures contract specifications2

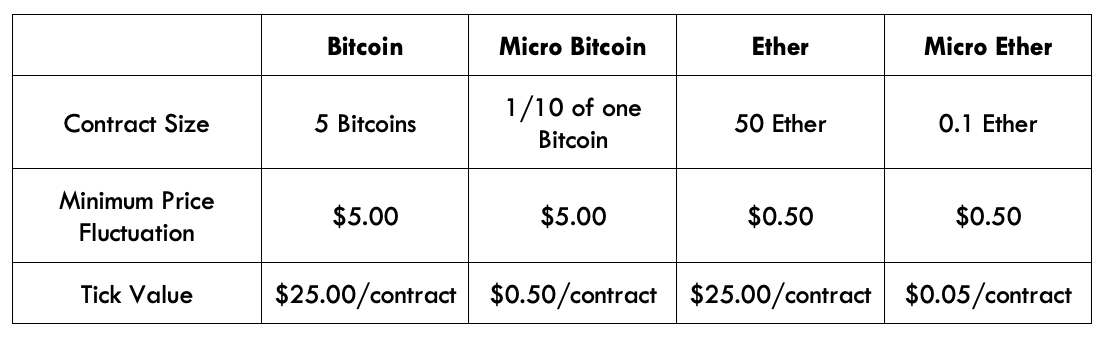

The CME has four futures contracts: Bitcoin, Micro Bitcoin, Ether, and Micro Ether3. Similar to other futures contracts, cryptocurrency futures contracts are all standardized. Bitcoin futures contracts will be used to help explain the contract specifications and then reference some of the differences between the other contracts.

Contract Unit

Each futures contract is equivalent to 5 Bitcoins. The “5” may be referred to as a multiplier. For example, assume Bitcoin is trading at $50,000 (the contract is quoted as one Bitcoin per US Dollar), then the contract is worth $250,000. In order to determine where the underlying is trading, the CME has created two indexes (there are similar indexes for the Ether contracts). The first is Bitcoin Real Time Index or BRTI and the other is the Bitcoin Reference Rate or BRR. The BRTI is a real-time index in order for market participants to gauge where the index is trading at any point in time. The BRR is a daily reference rate that is calculated as follows:

The value of one bitcoin at 4 p.m. London time (yes London)

The value of one bitcoin is derived from various Bitcoin spot exchanges4

The one hour before the 4 p.m. settlement time is broken down into twelve 5-minute intervals

The median is calculated for each of the 12 intervals

The average of the 12 medians is then calculated as the BRR

Trading Hours

As mentioned in the introduction, the spot cryptocurrency markets trade 24/7. Trading for the CME futures contract starts at 5:00 p.m. Sunday and stops trading at 4:00 p.m. Friday. There is a 60-minute break at 4:00 p.m. each day. All times refer to Central Time. The BRTI has similar hours.

(It should be noted that block trades and Exchange for Related Positions (EFRP) do trade 24/7.)

Minimum Price Fluctuation

The minimum price fluctuation is $5 per Bitcoin. Therefore, since each futures contract represents 5 Bitcoins, the tick value – or minimum value fluctuation – per contract is $25.00. For example, if the Bitcoin futures contract is trading at $45,200 and moves to $45,205, the value per contract will have changed by $25.00. There is no in-between price between $45,200 and $45,205 as per the contract specifications. Further assume that if the starting price was again $45,200 and the futures price went down to $45,195, then the value would have also changed by $25 per contract. What if the trader owns ten contracts? In either scenario outlined above, up or down in price, the value would have changed by $250. The following table highlights the four contracts and their minimum price fluctuations and tick values.

Last Trading Day

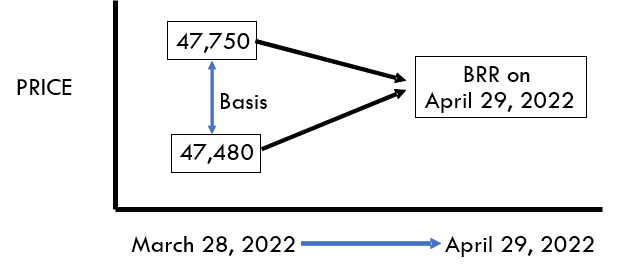

The last trading day of the contract is the last Friday of the contract month. For example, if today is Monday, March 28, 2022, then the last trading day for the April 2022 contract would be Friday, April 29, 2022.

Listed Contracts

There are six consecutive months listed plus the next two annual December contracts. Using the date from the last trading day in the above section, the next six months are April, May, June, July, August, September, and December of 2022. In addition, December 2023 will also be listed.

Daily and Final Settlement

Final settlement is based on the BRR. Daily settlement is based on the volume-weighted average price (VWAP) of CME Globex trades between 2:59:00 p.m. and 3:00:00 p.m. Central Time rounded to the nearest tradable tick.

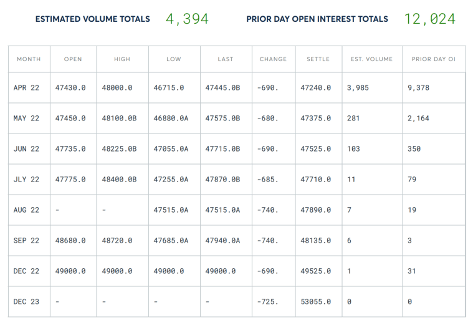

The following is a table showing the preliminary data at 5:00 p.m. CT as of March 30, 2022.

Source: cmegroup.com

Margin

Maintenance margins for Bitcoin are currently set at approximately $77,100 for the near contract and $86,500 for the contract with the longest maturity. This is approximately 32% and 36%, respectively, of the market value of the contract in today’s environment. Initial margin can either be 100% or 110% of the maintenance margin.

It is interesting to note, given the volatility of Bitcoin, that the margins are much higher than traditional instruments. For example, for the near contract the e-mini S&P 500, maintenance margin is 5.20% and the 10-year US Treasury note is only 1.3%!

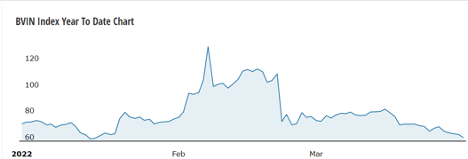

The Bitcoin Volatility Index (BVIN) gives us an idea of how volatile Bitcoin actually is. This chart shows the year-to-date implied volatility. Note the peak is approximately 130%!!

Futures are often used by market participants to speculate. Cryptocurrency futures are no different. If the trader’s forecast is for the value of the futures contract to increase, the trader buys or goes long the futures contract. If, on the other hand, the trader believes the value will go down, they will sell or go short the contract. In both instances, the assumption is made that the trader has no existing position or in market parlance terms, the trader’s position is flat.

Assume a trader buys ten contracts and, as in our prior example, the starting price is $45,000 and the forecast is for the price of Bitcoin is to go up. Now assume the price of the futures contract moves up to $45,200. The trader will have earned $10,000 which is calculated as:

10 contracts x the tick value of $25 x 40 – which is the number of ticks the price of the contract moved (200/5)

If, on the other hand, the forecast is for the value of Bitcoin to go down, then the trader will go short at $45,000. Now assume the value of the contract depreciates to $44,850. The trader will have earned $7,500 or 10 contracts x $25 for the tick value x 30 for the number of ticks that the price of the contract moved.

The above are for illustration purposes only as the trader could have easily lost the same amount of money!

Pricing

As with all futures contracts, the cost of carry needs to be taken into account. Simplistically, the formula would be:

Futures Price = Spot price + (Borrowing cost – Interest earned on the asset)

where both the borrowing cost and interest earned would be adjusted for the appropriate day count to match the maturity date of the futures contract. Since Bitcoin does not pay interest, the “interest earned on the asset” can be dropped from the formula. For the settlement procedure, (assuming no prices are available), the CME uses the following formula:

Reference rate + (Days to Expiration/365 x Interest Rate x Reference Rate)

where the reference rate is the Bitcoin Reference Rate (BRR) and the interest rate is determined by the CME. Backing into the interest rate yields approximately 8.00%. (Calculation not shown.)

Assume today is March 28, the April 2022 contract is trading at $47,750 and spot Bitcoin is trading at $47,480. The maturity date is April 29, 2022. The difference in the two prices is commonly referred to as the basis. The price of the futures contract should “converge” to the spot price on April 29 such that, in theory, there is no difference in the price. The following diagram illustrates the concept of basis and convergence:

If the BRR is $55,000 on April 29, then both prices should be $55,000. On the other hand, if the BRR is $45,000, then both prices should be $45,000.

Hedging

Hedging is the act of taking an equal and opposite position of the current position held by the trader/dealer/portfolio manager. Futures are an excellent tool for hedging. The question is how many contracts should be used to hedge the position.

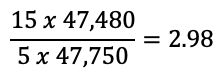

Assume a Bitcoin dealer owns 15 Bitcoins and wants to hedge with the futures contract. A naive approximation to determine the number of futures contracts to hedge with would simply be:

This would result in selling 3 futures contracts or 15/5.

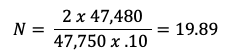

I might suggest that a more accurate formula can be used to determine the number of contracts:

Where N = Number of futures contracts required for the hedge.

Assume a dealer owns 15 bitcoins and the current price is $47,480. The dealer would like to hedge the position with Bitcoin futures. How many futures contracts should they sell?

Since futures deal in whole lots, the dealer would sell 3 bitcoin futures. This seems pretty straight forward and the reader might conclude “why not simply use the more simplistic approach?” If we change the example and now assume the target position is another cryptocurrency or even digital asset, the ratio would not be so clear cut. This is commonly known as cross hedging. In fact, we would need to add a correlation factor to come up with a more precise number of futures contracts to hedge with.

What if the number of Bitcoins owned by the dealer is less than 5 Bitcoins? For instance, what if the dealer was trying to hedge only 2 Bitcoins? Then, the Micro Bitcoin futures contract might be a better choice as the Bitcoin futures contract would end up with a position that is over (or under hedged depending on the amount of Bitcoin being hedged). The formula would be:

Rounding up the dealer would sell 20 Micro Bitcoin futures contracts

Who is using cryptocurrency futures?

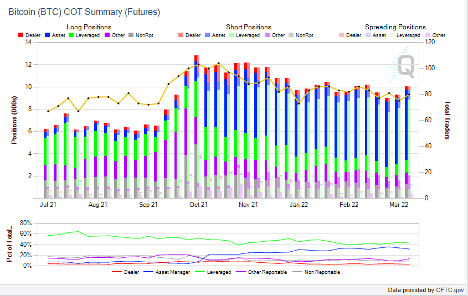

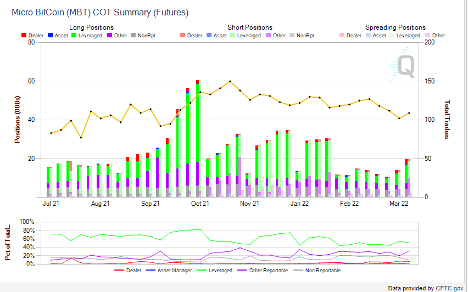

The CFTC provides a weekly report indicating what type of entities/institutions are using futures contracts. Below is the report as of March 22, 2022 indicating the entities using Bitcoin futures and Micro Bitcoin futures. In the first chart, it is interesting to note that in October 2021, cryptocurrency ETFs started to trade in the US. The primary underlying in these ETFs is the front-month CME Bitcoin Futures Contracts hence the big increase in asset manager’s long positions. Leveraged funds are the dominant short position.

However, in the Micro Bitcoin futures, leveraged funds dominate both long and short positions (potentially pointing to traditional long short strategies?).

Summary

Derivatives are now the majority of cryptocurrency transactions. Futures are one way of gaining exposure or hedging to cryptocurrencies. There are perpetual futures and fixed dated futures, regulated and unregulated futures contracts. We have analyzed the CME Bitcoin futures contracts and their use in speculating and hedging. And we concluded this article with who is using these contracts. In future blog/articles, we will look to examine both the spot and other derivatives markets including the perpetual futures contract.

References

1 There are other cryptocurrency futures exchanges. Some examples are FTX, BitMex, OKX and Binance.

Ken Kapner, CEO and President, started Global Financial Markets Institute, Inc. (GFMI) a NASBA certified financial learning and consulting boutique, in 1998. For over two decades, Ken has designed, developed and delivered custom instructor led training courses for a variety of clients including most Federal Government Regulators, Asset Managers, Banks, and Insurance Companies as well as a variety of support functions for these clients. Ken is well-versed in most aspects of the Capital Markets. His specific areas of expertise include derivative products, risk management, foreign exchange, fixed income, structured finance, and portfolio management. He has been a Risk Management Advisor to a Mutual Fund’s Board of Trustees and has served as an Expert Witness using knowledge of derivatives, trading and risk management.

Prior to starting GFMI in 1998, Ken spent 14 years with the HSBC (Hong Kong and Shanghai Banking Corporation) Group in their Treasury and Capital markets area where he traded a variety of instruments including interest rate derivatives, spot and forward foreign exchange, money markets; managed the balance sheet; sat on the Asset Liability Committee; and was responsible for the overall Treasury activities of the bank. He later headed up HSBC’s Global Treasury and Capital Markets Product training for two years in Hong Kong. Specifically, his responsibilities included developing new courses and delivering courses to traders, support staff and relationship managers. In New York, he established a training department for the firms’ Securities Division where he was in charge of the MBA Associates Program, continuing education and Section 20 license.

He has co-authored/co-edited seven books on derivatives including The Swaps Handbook and Understanding Swaps.

Publications and Articles

Articles

2019 3-Month SOFR Futures

2019 LIBOR Schmibor: What’s Next? SOFR Part I and Part II

2018 VIX, Volatilities, and Exchange Traded Products

2018 Settlement Risk and Blockchain

2017 Electronic Trading and Flash Crashes – Part I and Part II

2016 The Long and Short of IT: An Overview of XVA

2016 The Long and Short of IT: An Overview STACR and CAS

2016 The Federal Reserve Tolls: Past and Present

2016 The Perfect Storm: October 2008

2016 Interest Rate Swap Futures: An Introduction

2014 Risk Reversals

2002 Futures Magazine, Doing Your Homework on Individual Equity Futures (Co-written with Robert McDonough)

Blog

Ken also edits and writes for the GFMI Blog.

Books

1996 Como Entender Los Swaps, (co-author: John Marshall), published by CECSA (a Mexican publishing firm). This is a translated edition of our book Understanding Swaps, but with adaptations to fit the Mexican markets. (289 pages)

1993 The Swaps Market: 2nd edition, Kolb Publishing, 288 pages (co-author: John Marshall, copyright 1993). This book is directed to the graduate business student.

1993 Understanding Swaps, John Wiley & Sons, 270 pages (co-author John Marshall, copyright 1993). This book is directed to the practitioner market and is published as part of Wiley’s Finance Series.

1993 1993-94 Supplement to the Swaps Handbook, New York Institute of Finance, a Simon & Schuster Company, 494 pages, (co-authors John Marshall and Ellen Lonergan, copyright 1993). This book is directed to a practitioner audience and is a supplement to The Swaps Handbook. My role was largely that of editor.

1991 1991-92 Supplement to The Swaps Handbook, New York Institute of Finance (Simon & Schuster Professional Information Group), 300+ pages (co-author: John Marshall copyright 1992). This book is directed to a professional practitioner audience and is an annual supplement to The Swaps Handbook.

1990 The Swaps Handbook: Swaps and Related Risk Management Instruments, New York: New York Institute of Finance, a Simon & Schuster Company, 543 pages. (co-author: John Marshall). This book is directed to derivative product professionals.

1988 Understanding Swap Finance, Cincinnati: South Western publishing Company, 155 pages. (co-author John Marshall, copyright 1990). This was the first academic text published on the swaps markets.

Affiliations

International Association of Financial Engineers Board of Advisors – 1994 – 2010